How an ESG focus impacted fixed income returns in 2021

- 14 February 2022 (5 min read)

For bond investors, 2021 was very much a year of two halves. Early in 2021, the market backdrop was one of relative calm, buoyed by the imminent rollout of vaccines worldwide.

However, the reopening of economies across the globe brought its own set of challenges, as renewed demand for goods and services created an environment of rapidly rising inflation and increasing concerns over tighter monetary policy.

In addition, a new, highly transmissible COVID-19 variant – Omicron – arrived late in the year, bringing with it renewed fears over further restrictions being put in place and reduced economic activity.

By the close of the year, equities had delivered robust, above average total returns where the MSCI World NR Index delivered over 20%. In contrast the ICE BofA Global Government Index and ICE BofA Global Corporate indices achieved just -2.29% and -0.99% respectively over the 12 months.1

However, our analysis of bond performance in 2021 suggests that ESG screening may potentially be able to help provide a buffer for fixed income portfolios. Importantly, it also appears that applying such screening – as investors increasingly want to invest responsibly alongside their financial objectives – does not necessarily impact the potential ability for fixed income portfolios to outperform the broader market.

Taking the ICE BofA Global Corporate Index, we found that excluding bond issuers with a poor ESG profile allowed a simulated portfolio to perform in line with the market, while a simulated portfolio consisting purely of ESG leaders – bond issuers with the best ESG profiles, according to our methodology outlined below – marginally outperformed. Below, we explain our findings.

Exclusion bolsters performance

We believe a key part of responsible investing is avoiding issuers with high ESG-related risks. At AXA IM we employ a screening system – our Sectorial policies – across the majority our assets under management.

We exclude companies which fall into certain categories. These include controversial weapons, climate risk, ecosystem protection and deforestation, as well as soft commodities, where we aim to avoid short-term financial instruments which may contribute to price inflation in staples such as wheat, rice, or soy.

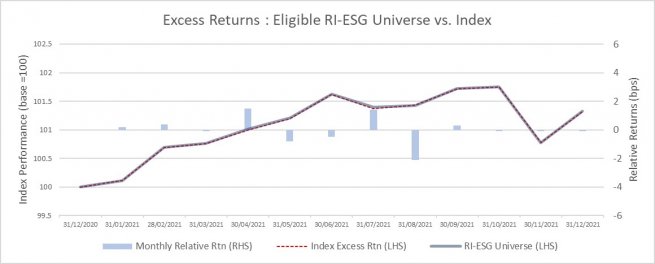

In addition, our ESG Standards policy has other exclusions based on severe controversies, white phosphorous, tobacco and low ESG quality. To address ESG quality in this instance, we applied our ESG scoring methodology to the ICE BofA Global Corporate Index (G0BC) to remove securities that scored below two out of 10. Overall, these actions removed approximately 10% of the benchmark universe.2

To test how performance was affected, we assessed the performance on a monthly basis using excess returns data – versus government bonds – at security level. Monthly rebalancing of the portfolio was conducted at sector level, ensuring that weight, spread duration and the average spread of each allocation closely aligned to the index, to remove the credit beta bias we observe in our scores.

Our analysis found that the performance of this simulated portfolio throughout 2021 was closely aligned to that of the benchmark universe, with less than one basis point (bp) difference in return profile over the full year. The largest monthly difference occurred in August, when the screened universe outperformed by two basis points (bps).3

This could suggest that applying ESG and Responsible Investment (RI) screening may open up the possibility for investors of keeping pace with, or slightly outperforming the broad market while also potentially adding some downside risk protection against ESG/RI related tail risks.

- Qmxvb21iZXJnIC8gRmFjdHNldCBhcyBhdCBlbmQgRGVjZW1iZXIgMjAyMQ==

- QVhBIElNIGFsdGVyZWQgaXRzIEVTRyBzY29yaW5nIG1ldGhvZG9sb2d5IGluIE9jdG9iZXIgMjAyMQ==

- U291cmNlIGZvciBhbGwgcGVyZm9ybWFuY2UgZGF0YTogQmxvb21iZXJnIChJQ0UgcG9ydGFsKSBhbmQgQVhBLUlNIChTQ0Q=

Assessing the ESG leaders

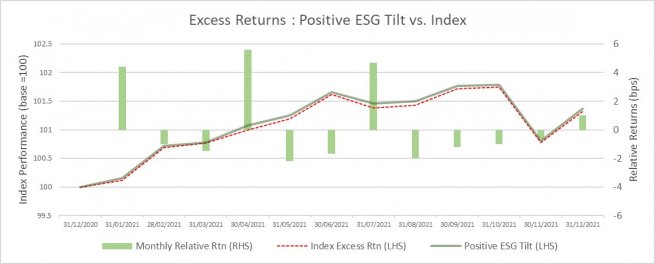

For a more refined version of this approach, we took the ICE BofA Global Corporate Index as before, and applied our AXA IM Exclusions and Standards policies – but then filtered for securities scoring five or higher according to our ESG Scoring methodology, which removed about 35% to 40% of the index.

This should help ease the tail risks associated with ESG factors, but also has the effect of tilting our portfolio to companies that typically score higher on such measures, versus the index. It is difficult to attribute relative performance to individual factors. But we can assess the performance of a portfolio with a materially higher ESG score than the universe, aligning sector weights, spread duration and average spreads to minimise key systematic risk differentials in an attempt to isolate the effect of ESG scores.

Once again, we assessed performance on a month-by-month basis using excess returns data at security level. We rebalanced portfolios monthly at sector level, ensuring that weight, spread duration and average spread of each allocation were aligned with the benchmark as closely as was reasonably possible. We found a small, albeit positive outperformance of the positively ESG-tilted portfolio versus the index: 137bps versus 132bps.

As was the case with our 2020 research, our 2021 analysis suggests that applying ESG and RI screening to our portfolios does not necessarily impact an investor’s ability to outperform the broad market. By applying such filters and ESG scoring, it can help deliver positive credit selection criteria, which can potentially contribute to overall performance.

ESG demand looks set to continue

Of course, past performance should never be used as a guide to future returns. But we believe that if a company has a high ESG score, this can act as a signal not only of ESG quality, but perhaps also of strong management and effective long-term strategy.

Certainly, the recent past has highlighted investors’ appetite for ESG investment strategies – notably a record $649bn flowed into ESG focused portfolios worldwide in 2021 (to end of November) – a significant rise on the $542bn and $285bn of inflows during 2020 and 2019 respectively, according to Refinitiv Lipper data.4

Fundamentally, we believe ESG analysis – and using this analysis in our investment process and decisions – can not only allow clients to align their portfolios with investment solutions that address global challenges, but also aim to create sustainable value for investors.

- SG93IDIwMjEgYmVjYW1lIHRoZSB5ZWFyIG9mIEVTRyBpbnZlc3RpbmcgKHRydXN0Lm9yZyk=

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.