Diversity: A competitive advantage?

New research from Rosenberg Equities suggests that diversity can act like a protective moat, enabling some highly-profitable firms to withstand competitive forces such as pricing competition and strains on talent retention better than their peers. Our research shows that the level of board diversity is not only associated with better current financial outcomes, but may also be a predictor of a company’s ability to protect future profits.

Why? We believe that more diverse firms most likely have an advantage when it comes to problem solving, which is at the core of the fight against competition. Specifically, that firms with more diverse leadership (defined as a Board Diversity score of over 20%, per Asset4) are better at developing strategies that act as a barrier to entry from competitors, counter the threat of substitution to the firms’ goods and services, and foster superior innovation.

By looking at data of the 1,000 largest US companies between January 2005 and July 2017, we sought to add to the existing body of work that highlights the benefits of diversity, and extend it into the realm of future earnings.

We found three key things:

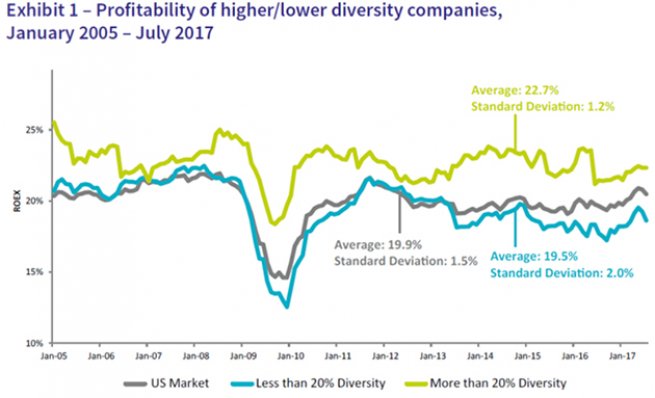

First, more diverse companies exhibited higher contemporaneous returns on equity, as shown in Exhibit 1. Importantly, not only were more diverse companies more profitable, the variability of that profitability was lower too. This was especially evident during the global financial crisis.

The third, and our key conclusion, is that board diversity may provide a ‘profitability moat’ to those firms that are already profitable and looking to keep competitive forces at bay.

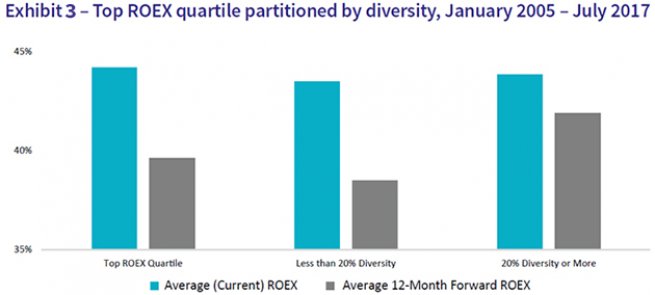

To measure whether or not diversity could act as a shock absorber, effectively nullifying some of the competitive pressures at work against profitable companies, we specifically looked at the top 25% of large US companies in terms of profitability. While all the companies in the top 25% faced considerable downward pressure on profits over the 12 months (as is only natural), those with higher diversity scores fared significantly better than those without. This is shown in Exhibit 3.

At a sector level, the ‘higher diversity, higher moat ratio’ rule generally held true too, indicating that our findings were more than just the result of specific sector bias. The three exceptions to the rule are Finance, Healthcare, and Industrials, though the first two appear almost equal. In all other sectors, higher diversity names appeared less subject to reversion-to-the-mean pressures (i.e. they have higher moat ratios) than lower diversity companies. Interestingly, among the most profitable group, companies in the Transport, Consumer Discretionary and Technology sectors that had higher diversity also had a moat ratio of greater than one, indicating that future profitability was actually higher than the already high current profitability.

As investors, our interest in diversity, governance, and ESG generally is grounded in the relationships we have found between ESG concepts and the fundamental drivers of risk and reward in the equity market. And, for those of us committed to diversity in the workplace, these results support the idea that diversity is not just a ‘nice to have’; we believe it is instead a ‘must have’ in the face of intense market competition.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.