Canada Outlook – reducing spare capacity

KEY POINTS

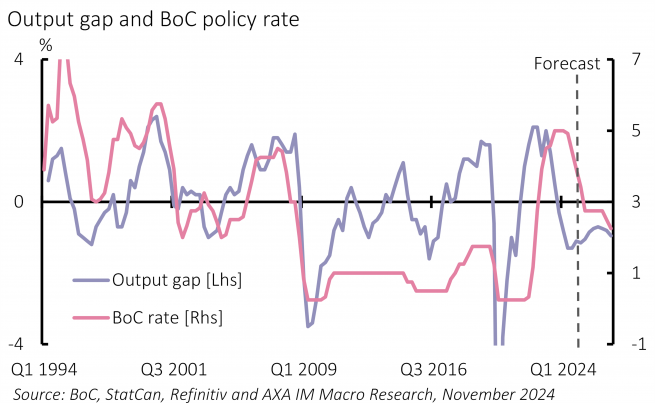

Canada’s GDP looks set to rise by 1.1% in 2024, in line with our view since April but quicker than forecast a year ago. Inflation has fallen faster with the headline at 2.0% and the core median rate at 2.4% – above target but much closer than we expected a year ago. This allowed the Bank of Canada (BoC) to ease policy faster than expected; it is forecast to end 2024 with a final 0.50% cut in its policy rate to 3.25%, 100 basis points (bp) more than we anticipated a year ago. The BoC estimates an output gap that reached 1.3% of GDP by mid-2024 as subdued growth fell short of a potential rate it estimates between 2.1-2.8%. It sees this adding disinflationary pressure. The BoC has been easing policy closer to neutral (estimated 1.75-2.75%) to close the gap and anchor inflation around target (Exhibit 10).

A number of factors should help narrow the output gap across 2025. First, we forecast growth to accelerate next year. There is some evidence the fast pace of BoC easing has underpinned a revival in consumer confidence and started to firm retail activity. Indeed, with the fading impact of the mortgage rate increase into 2025, the BoC’s cuts should soften the mortgage conditions headwind, while more subdued inflation should firm real disposable income growth. We remain cautious about business and residential investment outlooks. Yet we now forecast GDP growth accelerating to 2.1% in 2025.

This would not close the output gap alone but the BoC estimated a slowdown in potential growth to 1.1-2.4% in 2025 as temporary migrant workers fall and a more recent restriction to target 1.1m total migration between 2025-2027 should slow it further. Alongside our own weaker productivity estimates, these suggest potential growth towards the lower end of the BoC’s range, indicating less excess supply and tempering cuts. Inflation has fallen faster than we forecast reflecting globally familiar combinations of improved supply conditions, labour matching and energy markets. Inflation is on track to average 2.4% in 2024, but we expect this to fall further into next year, to average 1.7%, before rising to 1.9% in 2026.

As such we expect the BoC’s enthusiasm for policy cuts to fade early next year. We forecast the BoC to slow cuts to a 0.25% clip in early and expect it to stop cutting at the upper end of its neutral rate assessment – at 2.75% in March – as it recognises improvement in activity following its prompt easing, wary of the lags in monetary policy.

External developments are likely to be key, none more so than the US elections. The new US administration is likely to see a series of measures that further restrict the BoC’s space to ease policy further. US tariffs, which we expect to exclude Canada, should further boost spillovers of persistent solid US GDP growth into 2025. Moreover, a weaker Canadian dollar – currently around 20-year lows – should limit BoC divergence from the Federal Reserve.

Canada also faces its own election. While Prime Minister Justin Trudeau’s minority Liberal government could fall earlier, an election must be held by October 2025. Current polling suggests right-of-centre Conservatives led by Pierre Poilievre would emerge as the new government. Parties have not published manifestos but concerns about social spending would make a shift in the tax and spend balance likely, which could add headwinds to the 2026 growth outlook.

We expect growth momentum to soften in 2026, largely on the back of a slowing US economy and we forecast Canadian GDP growth of 1.7%. An externally led slowdown, with the economy still exhibiting spare capacity is likely to prompt the BoC to resume easing and we expect the policy rate to close 2026 at 2.25%.

Subscribe to updates

Have our latest insights delivered straight to your inbox.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.