Eurozone – High stakes amid political fracture risks

KEY POINTS

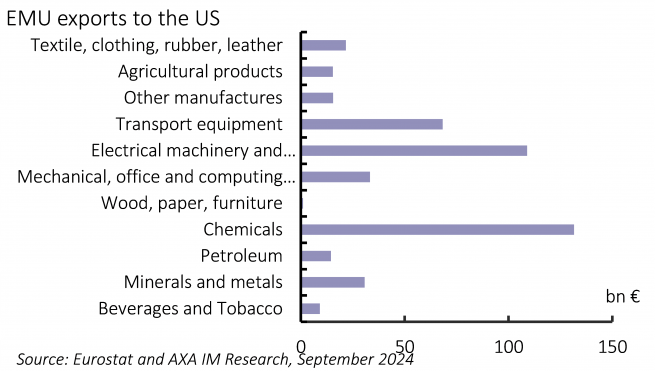

Trade tariffs: Marginal direct impact

The US election’s potential impact on the Eurozone is rather binary – a Kamala Harris victory is unlikely to have a material effect but a Donald Trump win would. Trump wants to narrow the US trade deficit and the Eurozone is a key contributor to this. The bloc exported €450bn of goods in 2023 (or 3.1% of GDP) (Exhibit 4), yielding a surplus to the US of €133bn.

If he were to secure a second term, Trump has proposed a blanket 10% tariff on the rest of the world, including the Eurozone. The weighted average of US tariffs on EU exports is around 3%, according to World Trade Organization data, implying a further 6.8% rise in export prices. Assuming an historical elasticity of around -1, we estimate it would reduce total Eurozone goods exports by €30bn (0.2% of GDP) – a rather limited direct impact. We note, that the bulk of eurozone exports gross value added to the US mainly consists of intermediate goods which may suggest some downside to historical elasticity. Such an impact should be further moderated by a depreciation of the euro against the dollar in response to domestic tariffs and other policy adjustments limiting the Federal Reserve’s space for cuts. This would likely lower the price of Eurozone exports, also potentially benefitting the bloc from increased competitiveness in non-US countries if they retaliate with increased tariffs on the US, but not on the Eurozone. Since the start of 2023, net trade has already added 0.2 percentage points (ppt) per quarter to Eurozone growth (0.0ppt in 2014-2019), with share of US exports up 8% – tariffs present a direct risk.

We see a bigger indirect risk if a second-term Trump trade policy starts a trade war between the three main economic blocks. Trump has been even more aggressive towards China, threatening 60% tariffs. At the risk of oversimplifying, Chinese exporters would likely try to find a substitute market with similar consumers to the US; Europe would be the natural target. A number of European industries, already in a tumultuous state, would face greater competition from Chinese producers, raising expectations of EU intervention with its own tariffs. Yet the current negotiation on Chinese electric vehicle tariffs has revealed challenges on this path. Reaching an EU majority is complex, as each country’s interests differ. Furthermore, political stability in the Eurozone has significantly eroded since Trump’s first term and key elections loom in Germany (2025), Italy (2026) and France (2027 at the latest).

For the Eurozone, global protectionist policies, together with associated economic uncertainty would likely affect domestic and foreign investment. The impact is difficult to estimate but would be crucial for both short and medium-term growth.

European security tensions

US support for Ukraine and implications for NATO are also a concern. Trump has claimed he would secure a swift peace deal in Ukraine. The fear is that this is an implicit threat of withdrawing support to Ukraine. The EU would not be able to replace the scale of US support – especially in the materials. This would raise concerns about US commitment to NATO and European security more broadly. In recent years, European countries have increased their defence spending, though still not all match their NATO pledges. A Trump presidency would likely push for this at least, but a perception of broader US security withdrawal may lead countries to raise defence spending more materially, something that would additionally strain vulnerable EU public finances and relations.

Fluctuations in energy prices may also impact the Eurozone. Increased US production and a deal with Ukraine may lower gas prices, but elevated Middle East tensions could boost oil costs.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.