Beating inflation

Tariffs are coming and this could mean higher US inflation, which is already above the Federal Reserve’s (Fed) 2% target. Reciprocal tariffs could raise inflation elsewhere. The 2% inflation gold standard for central banks feels out of reach right now, certainly in the US and the UK. This should be a concern for government bond holders. Returns should be positive in the near term but the last decade or so suggests that “risk-free” governments assets have not preserved real value very well. Equities and high-yield bonds tend to be better inflation-proof assets over the long term. As always, timing is important and diversification even more so. We live in a world where tail risks – recession and inflation – are bigger and we need to think about how we invest accordingly.

Inflation is the bogey

Inflation is the worst enemy of long-term bond investors. The nominal value of a bond starts to decline as soon as it is issued – because there is always some inflation. Indeed, economic orthodoxy argues that a small amount of inflation is desired – it oils the wheels of the economy and central banks tolerate modest inflation rates. The inflation shock of 2021 and 2022 did a lot of damage to bonds’ real value and bond portfolios’ real returns have been low or negative over the medium term as a result.

The current inflation picture is mixed. At the time of writing France announced that its inflation rate had fallen to 0.9% in February, the lowest for four years. Yet in the US and the UK, inflation is still running at 3.0%, a full percentage point over the generalised target of 2.0% for most central banks. At least real yields are positive and that compensates for the inflation impact on a bond’s capital value. But if investor expectations are anchored to central banks achieving 2.0% and the reality is that inflation gets stuck at 3.0%, then investors may eventually demand higher yields to compensate. For governments, with nominal liabilities, this inflation miss is a funding gift. With inflation risks to the upside – because of Donald Trump’s agenda, a less globalised world and a potential trade war – investors need to think hard about how to protect their portfolios over the medium term. Recent history serves us good food for thought.

Good and bad times

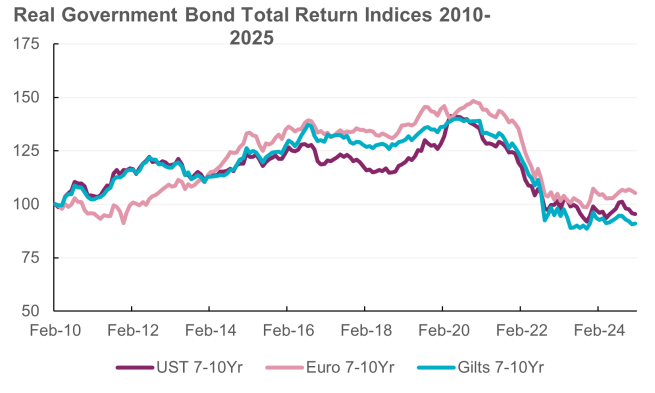

Bonds did a reasonable job providing positive real returns between 2010 and the beginning of the post-pandemic inflation shock (I am using April 2021 as a common starting point for that in the major economies). Across government, corporate and high yield bonds in US dollar, euros and sterling, real returns were positive and were higher the longer the maturity of the bonds held. For example, in US dollars, the annualised compound real return of the one-to-three year Corporate Bond index between the beginning of 2010 and March 2021 was 0.3% while for the seven-to-10-year bucket it was 4%, and for bonds with maturities over 15 years it was 5.6%. During that period central banks were actively bringing down bond yields and inflation was low. The same pattern is repeated for the euro and sterling markets. Note, I used headline consumer price indices as the deflator for each currency bloc.

The shock

However, on the eve of the inflation shock, yields were insufficient to cushion investors from the impact of rising prices. Real returns from government and some corporate bond indices, since April 2021, are still negative. This is not surprising given that inflation has been much higher, and bond prices fell significantly when central banks reacted. Only CCC-rated US high yield bonds managed to deliver a small 1.7% annualised return since April 2021. Some of the annualised real returns over the period are shocking: -8% for the US Corporate Bond 15-year plus bucket, -9.4% for the long end of the euro corporate market and -18.7% for long UK gilts.

Real returns positive again

More recently, fixed income has done better. Since the 10-year US Treasury yield peaked in October 2023, real returns are positive. The best inflation-adjusted returns have been in US high yield and longer-dated euro corporate bonds. Falling inflation and tighter credit spreads have helped boost real returns. As noted, several times recently, this has also meant more of the total return is coming from income and income returns are now positive once adjusted for inflation. It is also worth noting, in the US and UK where the Fed and Bank of England have been slower in reducing rates, short-duration returns have outpaced longer-dated bonds in terms of real returns. The US Treasury one-to-three year index has an annualised real return of 2.3% since October 2023 compared to 0.7% for the 15-year plus maturity bucket.

Vigilance about inflation: 3% is not 2%

Over the last 15 years fixed income real returns have been modest as the damage from the 2021-2022 inflation shock is taking a long time to repair. For bond investors today, the fact that inflation, in some economies, remains above central bank targets will be a cause for concern. Nominal yields in German Bunds barely exceed the current German inflation rate. Elsewhere, there is a positive gap but, worryingly, in some cases that gap has been closing. In the UK gilt market, for example, the gap between the five-year yield and the annual inflation rate was more than 200 basis points (bp) last September. It was down to 120bp in January. The recent US Treasuries rally has reduced the gap in the US government bond market as well. Economists tell us that there are upside inflation risks to US inflation from the Trump agenda of tax cuts and tariffs but bond yields are currently falling. This is a short-term boost to real returns but means the longer-term ability of government bonds to offer inflation protection will be challenged.

Diversify and beat inflation

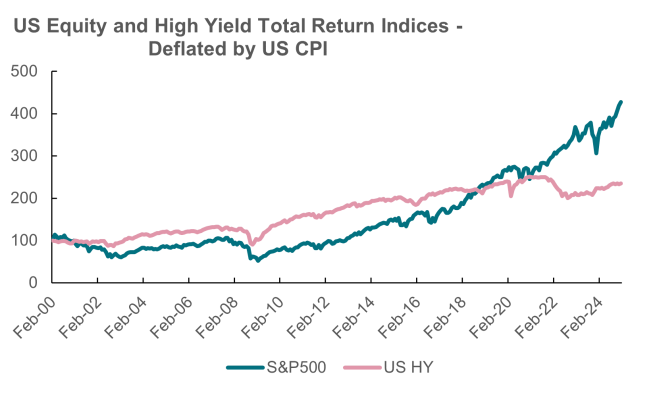

Beating inflation comfortably over the medium term has been best achieved in the past by investing in equities and credit, especially high yield. Exposure to corporate risk is beneficial, as companies adjust to inflation better than central banks can control it. Hence corporate cashflows retain real value. Doing the same analysis of inflation-adjusted returns for key equity markets shows positive returns across most time periods. In the 2010-2021 period, the S&P 500 had an annualised real return of 12.4% and since April 2021 it was 8.6%. Unsurprisingly, the Nasdaq 100 index has provided the best real returns since 2010 – the return on equity for technology companies has been a multiple of consumer price inflation, indicating an accrual of relative economic wealth to owners of technology capital. Technology and energy have also helped the Amsterdam stock index (AEX) generate the best medium term real returns amongst Europe’s key bourses (using the common EU inflation index as the deflator). Germany’s DAX has massively outperformed Bunds since October 2023 in the real return space (27% versus 5.0%).

High yield credit premium > inflation

High yield markets have also delivered positive inflation-adjusted returns most of the time. The additional credit risk premium over rates has more than compensated for inflation (and default risk). Of course, there will be times when this does not happen – in a recession when both equities and high yield suffer. In the previous 15-year period, which covered the aftermath of the dot.com bust and the global financial crisis, high yield real returns outperformed equities in the 2000-2008 period and then almost matched the very strong returns following the bail-out of the financial system from 2009 onwards. Both were extremely negative in calendar year 2008.

Uncertainties around the Trump economic agenda, US equity valuations, tight credit spreads and the potential for an increase in high yield default rates are staples of discussions about US markets. I have discussed equity valuations on a few occasions and recent price action suggests that matching 2024 total returns is going to be very challenging. It is noteworthy that consensus earnings growth forecasts have rolled over for the US and the ratio of upgrades to downgrades has turned negative. Bonds will offer protection if we are going into a risk-off phase and domestic market bonds will offer more protection from any kind of “buyer strike” on US assets. But longer term, high yield and equities provide the best inflation protection.

Near-term bond bullish

Tactically, I think bond yields could move lower. Being active in managing duration and asset allocation in fixed income is a way of combatting the structural drag on performance from higher inflation. It will be surprising to many that US Treasury yields have moved lower recently given the increased rhetoric around tariffs. I do not believe the bond market thinks the US Department of Government Efficiency (DOGE) is going to deliver massive structural declines in US federal government borrowing (the House just passed a bill paving the way for more tax cuts!). However, I do believe the bond market is telling us that downside economic risks are emerging. Three rate cuts from the Fed are now priced in. The relationship between the implied future cyclical low in the Fed Funds Rate and the current 10-year yield is a strong one. That low is currently 3.5% (by January 2027). If the market prices in two more 25bp rate cuts, a 10-year yield meaningfully below 4% could be on the cards.

Fat tails

It is a hard trading environment. Uncertainty is up and macro outcomes have fatter tail risks than before the election. For most investors, this means even more consideration needs to be paid to income generation and diversification. But we also need to consider long-term real value. In the short term, lower bond yields might be seen, but that just reduces longer-term expected real returns for buy and hold investors (which can include individuals holding government bonds in pension funds). My view is that investing in assets issued by the official sector has its limits and is inferior to holding diversified assets issued by the private sector, which is incentivised to be profitable even when there is inflation. The price of liquidity and credit risk free exposure in government bonds is, unfortunately, inferior real returns. The cost of taking on credit and equity risk usually outweighs the price of inflation. This also helps explain the surge of investment into private assets in recent years, where the recompense for taking liquidity risk is higher inflation-adjusted returns.

Addendum – the linker?

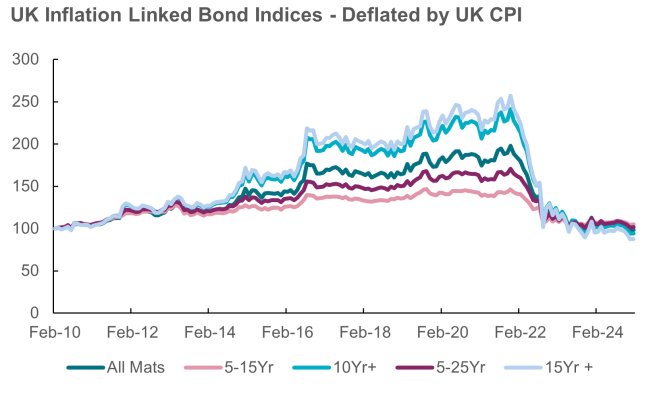

What about inflation-linked bonds (ILBs)? Of course, if you buy an ILB at issue and hold it to maturity, the value and the coupons received will incorporate inflation. However, inflation indices don’t always reflect this approach, and their mark-to-market valuation are impacted by changes in interest rates (typically ILBs are longer duration than their nominal bond counterparts, so are more sensitive to changes in rates). Anyone that held ILB portfolios through 2021-2022 will recognise the issue – real yields were very low by the end of quantitative easing, central bank tightening pushed them up, valuations suffered. Index return history does not paint a particularly satisfying picture as a result, as the chart of UK index-linked bond total return indices shows. Performance was hit by higher rates. Now that rates are closer to neutral, ILBs should do a better job in preserving real value. Inflation-linked bonds, along with credit, should form part of a fixed income allocation when beating inflation is the key investment objective.

(Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, AXA IM, as of 27 February 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Subscribe to updates

Have our latest insights delivered straight to your inbox

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.