CIO Views: Navigating Trump’s tariffs and interest rate risk in 2025

KEY POINTS

Chris Iggo, CIO AXA IM Core

Tariffs vs. investment returns

US President Donald Trump doesn’t like much about the global economic and political order. He feels the system has not treated the US well. This is exemplified by his frustration over the US’s net indebtedness position which, as of the third quarter (Q3) of 2024, stood at around $24trn. Years of large US trade deficits means the rest of the world has owned increased amounts of dollar assets. His tariff focus is seen as one way of addressing what is perceived as an unfair global trade system.

Capital flows into the US, as the counterpart to trade deficits, have gone into US Treasuries, real estate, direct investment in US companies and listed equities, exchange-traded funds and mutual funds. The bigger the trade deficit, the larger the capital flows with foreign investors taking comfort in the reserve currency status of the dollar. What if tariffs do cut the trade deficit? Capital inflows should ease too. In recent years flows into US equities have been significant (foreigners bought $230bn in Q3 2024 alone). There is a circularity here – inflows boost stock returns; high returns attract inflows. The US has outperformed as a result. If the flows diminish, the valuation gap between US markets and the rest of the world could be reduced. As the old saying goes, be careful what you wish for.

Alessandro Tentori, CIO Europe

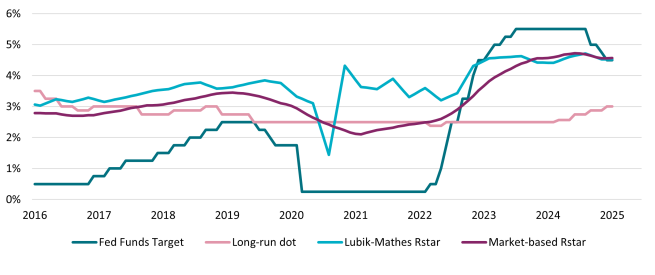

Neutral interest rates and the allocation of risk

The European Central Bank (ECB) recently estimated that the nominal r* – the short-term interest rate which would prevail when the economy is at full strength and inflation is stable – spans a range of between 1.75% and 3%. While it admits these estimates are subject to uncertainty, they are not inconsistent with the simple approach of deriving the neutral interest rate from structural variables. Currently, the sum of the Eurozone’s potential growth and the ECB’s 2% inflation target matches the ECB’s main deposit rate of 2.75%.

In the US, both market and (some) model-based estimates of r* provide us with information about the Federal Reserve’s (Fed) policy stance. The chart shows these estimates together with the Fed Funds Rate target as well as US policymakers’ own assessments of the long-run interest rate (i.e. the “dot”). At 4.50%, the Fed might be close to a neutral level – though this view is not yet shared by all of its members. The long-run dot lags significantly behind the recent, steep increase in policy rates and both estimates of r*. Furthermore, the simple approach mentioned earlier results in a neutral rate around 3.50%, about 50 basis points higher than the long-run dot.

The art of monetary policy making cannot, and should not, be reduced to a single equation - but there is value in factoring in this approach into our view on future interest rates and the allocation of bond market risk.

Ecaterina Bigos, CIO Asia ex-Japan

China’s economy needs more than AI

The emergence of DeepSeek - a rival to the popular ChatGPT - has been a gamechanger in terms of China’s position in the artificial intelligence (AI) race. It has bolstered investors’ optimism about the potential growth and economic benefits of AI – it’s widely believed AI adoption has the scope to boost earnings over the long term, via productivity gains, cost savings and likely new revenue opportunities. However, it’s early days in terms of real-world applications. For now, AI model training remains the primary focus. But risks are vast, such as those around AI data usage, industry regulation, national security, technology export controls, and the transferability of open-source models to existing ecosystems. The language in which models are trained is another key consideration, with Chinese companies naturally preferring domestic models.

The DeepSeek breakthrough indicates that innovation is likely to come from a broader group of players. And it is not unprecedented given that China has created tech giants that replicate global success stories in areas like e-commerce, search and social media. But China’s recent market rally is narrowly focused and narrowly driven; policy support is still required to address deflation, to drive a broader, sustainable earnings recovery. Demand-side policy support and signs of a more market-friendly policy shift towards technology companies are encouraging, but much more is needed to shore up confidence in consumers and investors, as well as in the private sector.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

CIO team opinions draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Rates | Medium-term rate expectations are stable but subject to policy triggered volatility | |

|---|---|---|

US Treasuries | Fed on hold until more clarity on inflation and Trump policy; bonds in range | |

Euro – Core Govt. | Range trading while markets wait for any new policy initiatives on the fiscal side | |

Euro – Peripherals | Spreads to remain narrow; focus on what eventual new German government will do | |

UK Gilts | Investors unsure about path of inflation and fiscal policy; gilts range bound for now | |

JGBs | Markets still expect further interest rate hikes | |

Inflation | Scope for breakeven rates to move higher as inflation continues to be sticky |

Credit | Credit remains strong with spreads stable and positive returns | |

|---|---|---|

USD Investment Grade | Strong earnings backdrop supportive for US corporate debt | |

Euro Investment Grade | Demand for fixed income remains strong; fundamentals are solid | |

GBP Investment Grade | Spreads have narrowed in 2025, but demand remains strong | |

USD High Yield | Solid economic data, strong cash-flows and technical factors continue to support high yield | |

Euro High Yield | Resilient fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Spreads over US Treasuries are attractive but Trump agenda could be disruptive |

Equities | Growth backdrop supportive but risks of tariffs hitting global trade | |

|---|---|---|

US | Earnings momentum starting to flatten; valuations are still expensive | |

Europe | Modest pick-up in earnings forecasts and possible beneficiary of global move away from US | |

UK | Markets need to see how government can improve growth prospects; lower rates will help | |

Japan | Solid combination of valuations and expected earnings growth | |

China | Tech sector bolsters investor optimism, with scope to broaden out on policy support | |

Investment Themes* | Competition in AI to create more opportunities for technology beneficiaries |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

Subscribe to updates

Have our latest insights delivered straight to your inbox

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.