Why ETF Fixed Income investors should consider a Paris-Aligned Benchmark

Key points:

- Providing a comparison for climate-related investments

- Characteristics similar to that of the Parent index mean there should be little trade-off for using a Paris-aligned Benchmark

- Some sector biases to reflect the need to meet the carbon targets.

-

A Paris-Aligned Benchmark offer active ETF funds with a climate-focused approach a spring-board from which to reflect the fund’s specific ESG criteria.

Identifying suitable benchmarks for ETF fixed income funds with carbon emission criteria has not been a straightforward task. While benchmarks exist for comparing impact bond portfolios such as green and social bonds, it has been challenging to find a reference point for a conventional bond portfolio designed to support the transition to a sustainable economy.

Now however, investors have two benchmark options: Paris-Aligned Benchmark (PAB) and Climate Transition Benchmark (CTB) which give particular emphasis on companies actively involved on decarbonisation efforts. The introduction of these benchmarks reflects the growing demand by investors to have the ability to align their investments to climate-aware goals.

The European Commission has established a framework for sustainable finance, enabling investors to better align their climate-conscious investments with the goals of the Paris Agreement. This framework, which includes tools like the EU Taxonomy, doesn't just promote a shift from fossil-fuel reliant activities to green ones, but also emphasises investments in transitioning sectors towards greater sustainability.

Paris-Aligned benchmarks (PABs) evaluate the alignment of investment portfolios with the objectives of the Paris Agreement, while Climate Transition benchmarks (CTBs) assess their contribution to the transition to a low-carbon economy. While both PAB and CTB share a similar focus on decarbonisation with an annual 7% target on carbon reduction, there are key differences between the two:

- The Paris-Aligned Benchmark (PAB) aims to achieve alignment with the 1.5°C goal of the Paris Agreement

- As such, the PAB approach excludes fossil-fuel intensive companies while CTBs focus on transitioning to a low-carbon economy rather than just limiting global warming

- PAB also requires a more aggressive 50% minimum carbon reduction relative to the market index, as compared to the 30% reduction required for the CTB approach.

How they help create an appropriate climate-aware comparison

With growing demand for Paris-Aligned Benchmarks (PAB), index providers such as MSCI, Bloomberg, ICE BofA, added new sets of corporate bond climate indices. These indices are climate variants of their corporate bond parent indices.

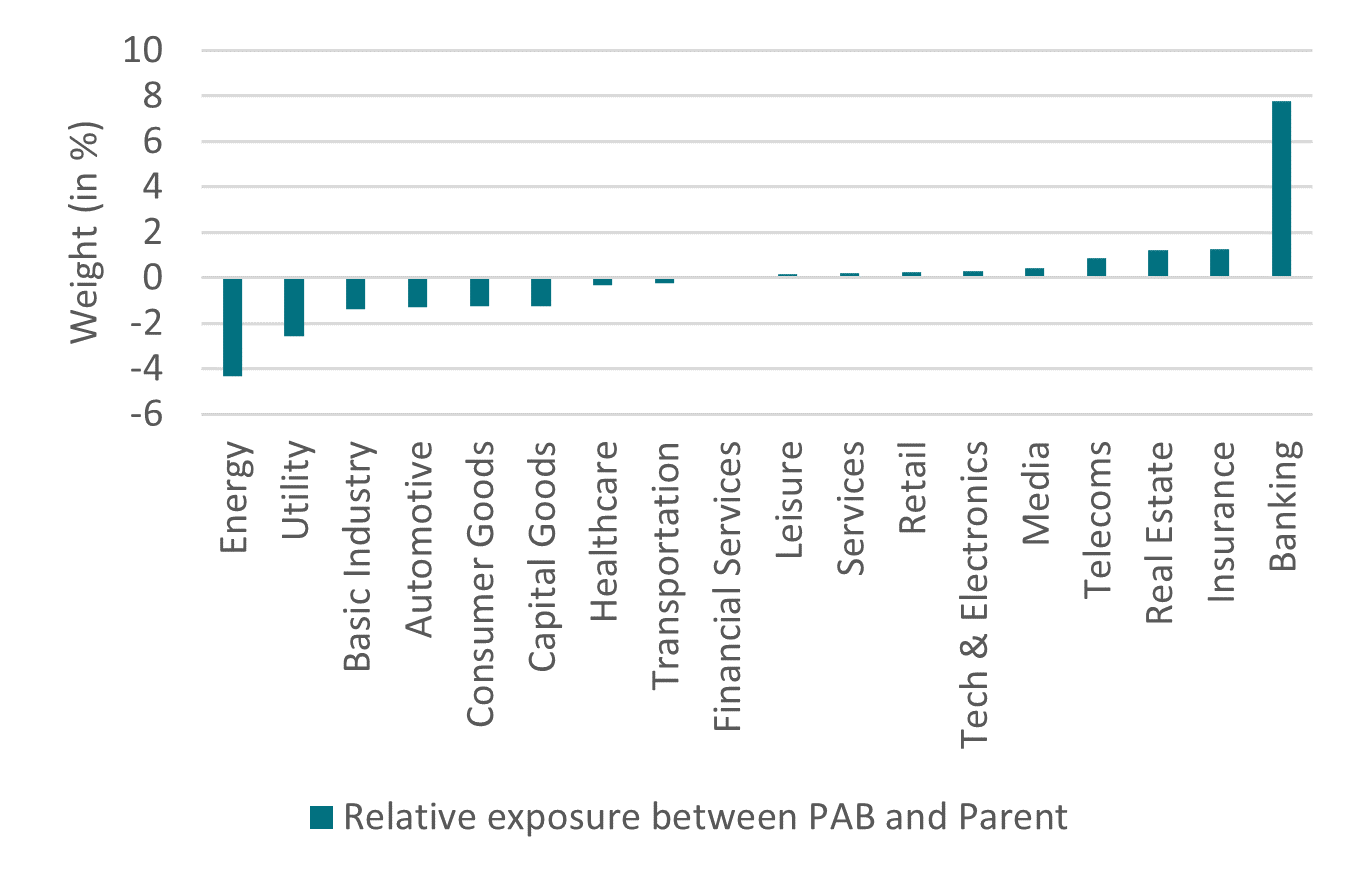

The PAB is designed to align with climate goals, typically emphasising sectors and issuers that contribute positively to decarbonisation efforts. The PAB, therefore, has a slightly higher weighting to lower carbon intensity sectors such as Banks, Insurance, Real Estate and Telecoms. On the other hand, it has less exposure than its parent index to other sectors that are highly carbon intensive such as Energy, Utilities and Basic Industry.

However, an important point to note is that it isn’t just a simple blanket exclusion within the benchmark for such sectors – by including these sectors but limiting the issuers within it, the benchmark aims to help fund the transition to a sustainable economy while encouraging issuers in more pollutant sectors to develop more sustainable practises.

Nevertheless, as the chart below demonstrates, the sector weighting differences between the PAB and its parent index remains limited.

Sector relative exposure

Source: AXA-IM, Bloomberg, as of 18/09/2023. Indices compared: Parent: ICE BofA Euro Corporate Index and PAB: ICE BofA Euro Corporate Index Paris Aligned (Absolute Emissions)

Is there a trade-off for a climate aware approach?

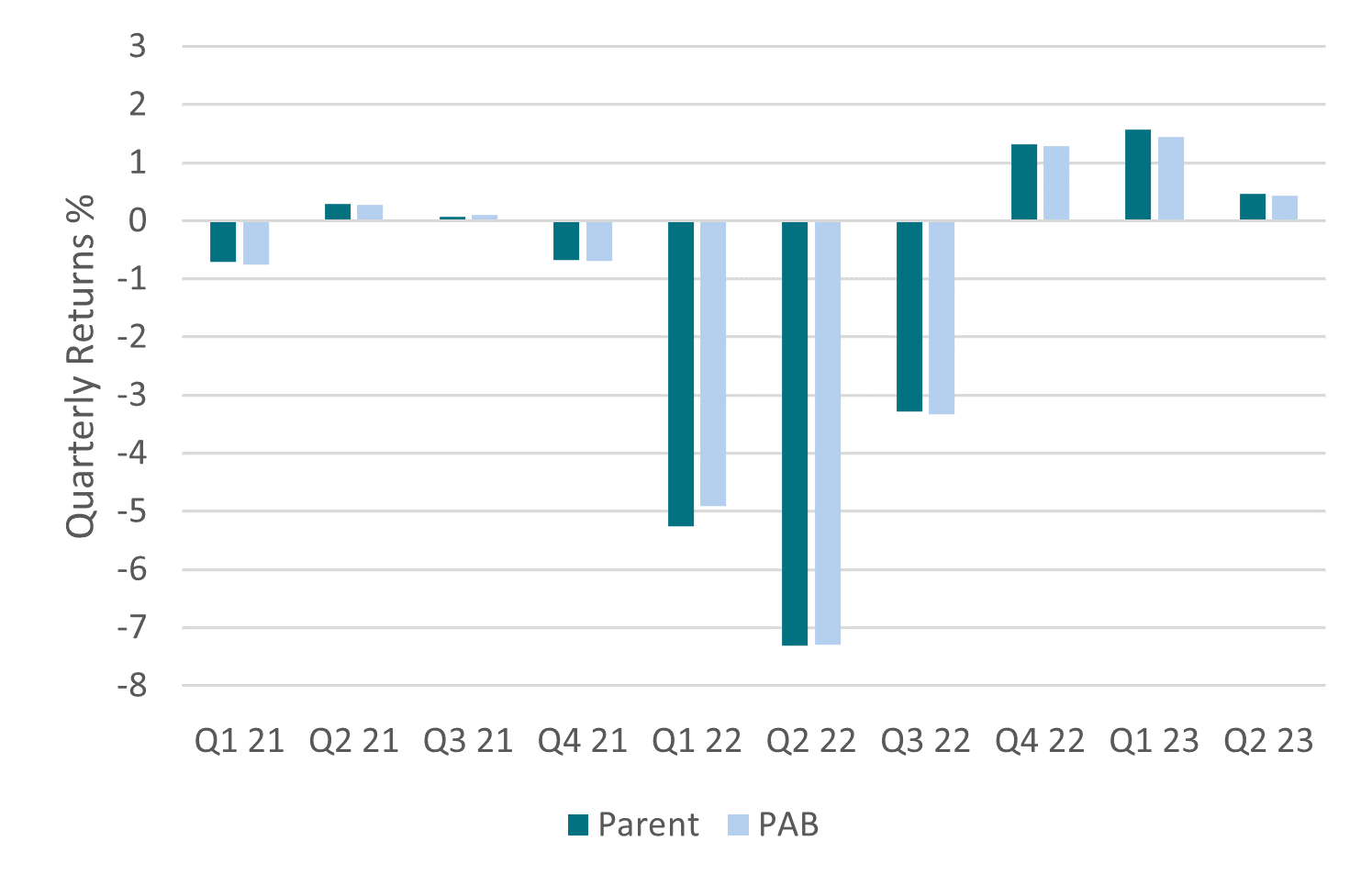

The role of a climate index is to closely track its parent index while sifting out issuers that don’t meet the emission requirements. Therefore, the climate index will have less issues than its parent index, although it still maintains sufficient diversity and liquidity.

When comparing the ICE BofA Euro Credit Paris Aligned (Absolute Emissions) index with its parent index, they both have similar credit risk profiles with each currently offering an average credit rating of A-.

Furthermore, the performance in 2021, 2022 and 2023 year-to-date was relatively closely correlated. While the data is still limited for comparison given that the PAB was only launched in 2021, these initial years demonstrate that it is possible to not give up returns for sustainable investing, as illustrated in the chart below:

Return for Parent and PAB indices

Source: AXA-IM, Bloomberg, as of 18/09/2023. Indices compared: Parent: ICE BofA Euro Corporate Index and PAB: ICE BofA Euro Corporate Index Paris Aligned (Absolute Emissions)

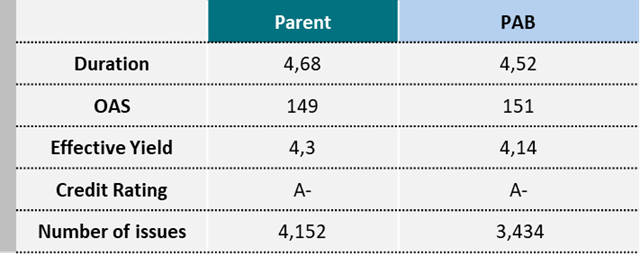

Overall, key characteristics remains similar between the PAB benchmark and its parent index:

Index Characteristics

Source: AXA-IM, Bloomberg, as of 16/08/2023. Indices compared: Parent: ICE BofA Euro Corporate Index and PAB: ICE BofA Euro Corporate Index Paris Aligned (Absolute Emissions)

We would argue that a PAB is an appropriate benchmark to use for active ETFs that are climate-focused. However, while there are still limitations on data for certain indices, we believe intellectual capital through an active approach is necessary. Therefore, while our analysts cover all the names in the benchmark, if they believe any issuer does not meet our own metrics, we will not invest. As part of this process, we also add benefit by meeting with the companies we invest in and having regular discussions to understand their business strategy. Therefore, active ETF funds reflecting the decarbonisation goals of a PAB offer investors the ETF benefits, such as transparency and liquidity, while providing the added-value of robust investment analysis.

A Paris-Aligned Benchmark is a well-regarded option for investors to use for their ETF fixed income investments. Comprising of conventional bonds instead of sustainable bonds, it offers investors a way to address their climate-related requirements across a broad range of fixed income portfolios.

References to companies and sector are for illustrative purposes only and should not be viewed as investment recommendations.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.