Multi-Asset Investments Views: Midnight oil

KEY POINTS

SpaceX’s initial public offering saw the company valued at about $1.8 trillion, which propelled it into the world’s top 10 firms by market capitalisation. It marked a pivotal moment for public equity markets and the artificial intelligence ecosystem.

As the first AI‑adjacent mega‑IPO, ahead of expected listings by Anthropic and OpenAI, the transaction highlights both the depth of demand and investors’ willingness to back long‑dated growth stories.

Nonetheless, it bears several hallmarks of late‑cycle excess. Retail participation reached an unprecedented 20% of allocations, with the transaction oversubscribed roughly threefold.

Meanwhile the circa 100 times trailing sales valuation underscores that pricing is almost entirely driven by belief in the long‑term potential (satellite-based internet, AI infrastructure, and space economy expansion) rather than observable fundamentals.

More broadly, it signals a shift in the AI narrative, from a fundamentally driven earnings story towards an increasingly technical and positioning‑driven dynamic.

The prolonged semiconductor rally

Nowhere is this more evident than in semiconductors, where the ongoing rally is no longer purely anchored in earnings upgrades but is amplified by structural flows.

Leveraged exchange-traded funds, single‑stock leverage and options‑related hedging flows are creating mechanically pro‑cyclical demand, forcing market participants to buy into strength and sell into weakness.

In parts of the semiconductor ecosystem, particularly in memory stocks, leverage‑induced feedback loops are becoming a dominant driver of volatility. On days when there are large market movements, dealer rebalancing flows can reach significant proportions of market liquidity, further exacerbating intraday swings.

While we believe AI’s structural case remains intact, these dynamics warrant caution. This prompted us to take profits on emerging markets equities, whose year-to-date performance has been largely driven by semiconductor stocks.

The combination of elevated retail participation and mechanically amplified flows suggests that pockets of the equity market are becoming more fragile, with volatility likely to remain structurally higher.

Earnings growth broadening

Beyond AI, market breadth is improving and supports our constructive stance. Positioning has normalised, sentiment remains only modestly above neutral, and our quantitative indicators continue to signal a supportive backdrop.

Singularly, some of the market’s traditional anchors within the so-called ‘Magnificent Seven’ are bearing the brunt of the recent capital rotation and valuation compression.

As these stocks have tended to act as a funding source for the AI trade, their underperformance has weighed on the S&P 500 relative to other segments of the market, prompting us to take advantage of the cheapening and rotate part of our US exposure back to the blue-chip index.

Fundamentals remain strong. The first quarter earnings season delivered exceptional results, with S&P 500 large caps posting around 28% year‑on‑year growth on average.1

Momentum remains intact, with the market consensus now expecting above 20% earnings-per-share growth for Q2, ahead of the reporting season starting in the second half of July.

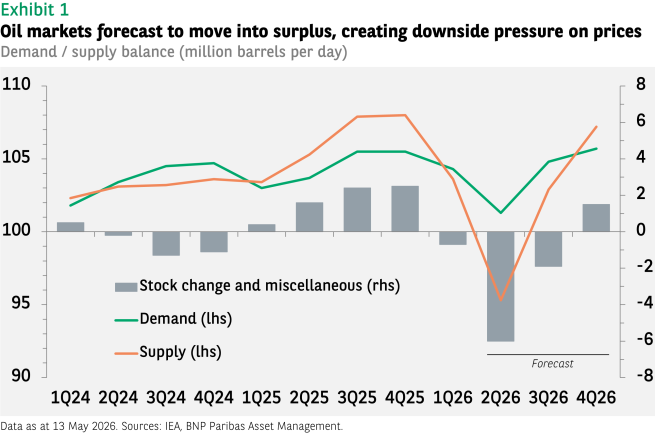

While technology should again be a key contributor, earnings growth is broadening meaningfully across sectors. In Europe, it is expected to return to double‑digit territory. While higher oil prices may weigh on Q2 results, we expect markets to look through any temporary weakness, provided confidence in the energy outlook stabilises.

Within the region, we favour Eurozone banks, where the combination of late‑cycle dynamics, elevated market activity and resilient growth continues to support the earnings outlook.

Crucially, the dominance of the AI narrative has overshadowed a meaningful broadening in market leadership. US small caps are a case in point, with the Russell 2000 delivering its strongest relative performance versus the S&P 500 since 2010, supported by robust earnings momentum.

This broadening reinforces our view that the current bull market is becoming more balanced, even as pockets of excess build up within AI‑linked segments.

- Source: Factset. EPS growth S&P for Q1 2026.

Central bank shifts

Kevin Warsh’s debut as Fed Chair marked a clear shift in communication, with a more assertive tone emerging alongside a hardening of hawkish positions within the committee. While recent data on consumption, employment and income growth justify the Fed’s renewed hawkish bias, we believe it can afford to stay on the sidelines for the time being.

Inflation is still running slightly above the central bank’s year‑end projections, but the trajectory should improve as lower energy prices feed through in coming months.

Markets have started to reflect this recalibration. The US yield curve has flattened, and the dollar has regained support. From a valuation perspective, the currency still appears fundamentally undervalued and could strengthen further as risk premia compress and lingering concerns around policy credibility fade.

In contrast, the ECB delivered its first rate hike since September 2023, signaling rising concerns over the broadening impact of the energy shock. The emphasis on potential second‑round effects reflects a more reactive stance, in our view.

We see this renewed hawkishness as somewhat misplaced given the absence of any clear evidence of persistent inflation, especially in wages. This hawkish policy stance offered an opportunity to buy euro duration.

We thus maintained a constructive position on five‑year German Bunds, expressing the view that market pricing for further tightening beyond one further hike was excessive. As expectations adjusted lower to below one hike by year-end, we closed the trade and reverted to a neutral stance on duration.

Overall, while central bank communication has become more hawkish on both sides of the Atlantic, we see limited scope for sustained tightening for now, especially in the eurozone.

The asymmetry likely remains in favour of stabilisation rather than further policy tightening, particularly should disinflation resume with oil prices returning to pre-Middle East conflict levels.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.