Mind the gap

The gap between realised inflation and the contemporaneous level of bond yields has never been higher. Bond markets might be telling us not to worry about inflation, it’s all transitory. But even if inflation settles lower, consistent with central bank targets, bond yields are *arguably* still low. A gradual withdrawal from bond buying might be what is needed to get yields higher. A 2.5% 10-year US Treasury yield is not out of the question should the Fed taper (as they will) and raise rates (as they will) in 2022. But we should consider what the consequences of inflation being higher for longer might be.

Higher yields…

There are good reasons why bond yields should be higher. The fact that they aren’t deserves some consideration in order to weigh up whether portfolios need to be adjusted to protect against higher yields and the potential that could have for risk premiums in credit and equities. The 6.2% increase in US consumer price inflation in October was at the 88th percentile of all year-over-year rates of change since 1953 yet bond yields are only at the 2nd percentile and the effective Fed Fund rate is even lower. The break-down between contemporaneous inflation and interest rates is similar in the Euro Area and in the UK. Historical relationships point to bond yields being higher and monetary policy being tighter. At all other times since the 1950s that US consumer prices have risen by more than 6% in a 12-month period, 10-year Treasury bond yields have been above 7% at the same time. See the chart below, the blue dot at the bottom of the 6%-7% range is where we are today in the US. Of course, the world is different today to how it has been in the past, but there is a fundamental relationship between long-term interest rates and inflation that has broken down over the last decade and is now at an extreme misalignment.

…maybe

It’s one thing saying where bond yields should be and quite another understanding why they are not. Successful investors don’t just bark “policy mistake” at central bankers but try and guess what the parameters of the reaction function are and, importantly, how other investors react to any changes. What squares the circle between where inflation is, and the current level of nominal bond yields is deeply negative real yields. The current market measure of 10-year real yields from the US TIPS market is -0.96%. The ex-post US real yield (nominal yields a year ago relative to realised inflation) was -5.5% in October. What investors need a view on is why real yields are negative. And of course, this is not just a US phenomenon – German real yields are -1.9% (the inflation linked German government bond maturing in 2033) and UK real yields for the 10-year inflation-linked gilt are -3.1%.

Freedom from repression!

I’ve written about this before. There are few empirically strong theories for why real yields are so low. It might be just because of quantitative easing which central banks resorted to in the absence of the ability to take short-term rates deep into negative territory. If central bank reaction functions are about to be re-calibrated to higher inflation and asset purchases come to an end, then short-rates and real-long term rates might move up. This surely is the playbook for bond bears. Central bank financial repression has pushed bond yields down to fundamentally mis-priced levels, so if you take away the financial repression, yields rise. And inflation is the macro reason we don’t need financial repression anymore.

Technical factors

With my fixed income colleagues I have been looking at market developments through the framework of considering macro, valuation, sentiment and technical factors for well over 10-years now. Increasingly, “technical” have dominated movements in yields and spreads, often contrary to the macro signals. But they are hard to measure. In practical terms it’s about trying to understand the supply and demand for fixed income assets that have more persistent influences on prices than just reactions to economic data releases or comments from central bankers. The biggest “technical” of them all in recent years has been central bank buying. Realistically, that has to stop before we see global real and nominal yields higher.Of course, bond yields might be low simply because – collectively – investors don’t think the current increase in inflation can persist beyond the next few quarters. Implicit in that is an expectation of limited monetary tightening and the world being far away from the complete removal of financial repression. Today’s news about a new COVID variant has created a sharpy risk-off move in anticipation of potential further disruptions to global trade and activity. It’s too early to judge, according to scientists, whether the new variant detected in southern Africa will be able to evade current vaccines, but clearly this is the risk. A new wave of lockdowns and falling activity would clearly push bond yields LOWER and delay the reckoning discussed in the rest of this note.

New equilibrium?

But what if? What about a scenario in which inflation does moderate over the next year and settles – in the case of the US – in the 2%-3% range. For Europe that would be closer to the 2% than the 3% level. Historically, inflation in that range has been associated with yields (10-year Treasuries in this case) anywhere between just under 2% to 8%. Since the 1950s, when US CPI inflation was in that 2%-3% range, the average bond yield was 2.5%. Funnily enough, that is where the Fed’s current estimate of the long-term neutral Fed Funds rate is. Yields at 2.5% over the next year would not be out-of-whack with fundamentals. Unless the technical forces are stronger than we think, investors should be prepared for that.

Active protection

The first investment implication is that fixed income portfolios need to be managed actively. A 100bp increase in 10-year yields would mean a negative price adjustment of roughly 9% on the current benchmark bond. Yields aren’t likely to move higher in a straight line, however, and actively managing duration, yield curves, inflation and cross-market spreads can deliver much better returns when markets are going through a valuation adjustment. Any such adjustment is likely to be more muted in European government bonds as the ECB will remain a buyer for some time, while there is likely to be more total return volatility in the UK gilt market given the longer-duration of the market indices, the unpredictability of the Bank of England and the likely worse inflation/growth trade-off in the UK relative to other major economies.

Sound credit

Higher risk-free yields and less central bank liquidity is likely to impact on credit spreads as well. Risk premiums should rise. However, the historical pattern is not clear. In the US the Fed tightened in 2004-2006 but investment grade spreads actually went lower. In 2015-2018, spreads rose in anticipation of Fed tightening but peaked within weeks of the first hike – and there were eight more hikes ahead. Spreads fell through that period. The bottom-line is that credit spreads only really widen when there is a growth or other systemic shock. At the moment, fundamentals remain good for most credit asset classes. It would be only if markets got very concerned about growth would credit suffer noticeably.

Stocks and higher rates

If yields rise, what does it do for equities. When Treasury yields rose to 3.15% in December 2018, the S&P500 was trading on a price-earnings ratio of 15.5x. Thus, the earnings yield gap was 3.3%. Today it is around 3%. Assume an earnings yield gap of 3% and a bond yield of 2.5%, that translates to a PE of 18.2x. On the basis of the current 12-month forward forecast for EPS of $217, that delivers a price target for the S&P of 3950 – 15% lower than today’s index level. But, like for credit, growth is the real driver of equities and investors might be happy with a lower earnings yield gap – they have been in the past.

Earnings remain key

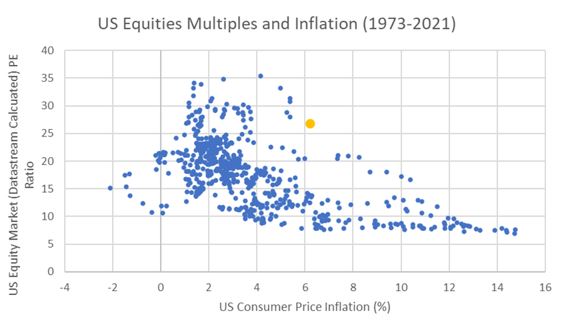

Equities face the headwinds of higher inflation, higher discount rates and a worsening relative valuation. Historically, equity multiples have fallen as inflation has moved higher and the 1%-3% range of inflation has been seen the market attach the highest multiples to earnings. Of course, higher inflation in the past was associated with higher bond and higher earnings yields. Low yields and strong earnings growth support equity returns for now. Having said that, investors might want to be tilted towards quality growth. I would think that energy comes off the boil next year, financials may still derive some support from the modest steepness in the yield curve, but cyclicals may struggle to maintain profit margins if cost increases persist. The green investment theme will also be a driver especially as the economics move irreversibly in favour of more sustainable business models.

Look to Asia

Other themes that could be interesting would be a rebound in Chinese and Asian markets. China’s growth slowdown is well known now, and the drama of the Common Prosperity announcements has passed. There are still issues with the property sector and that could have broader economic consequences – construction materials, labour, home furnishing and white goods demand. Onshore Chinese equities have performed better than the H-shares listed in Hong Kong but have still only delivered a total return to date of 6.3% (Shanghai Composite to 23-11-2021) compared to 23.6% for the MSCI World index. Domestic support for Chinese brands, investment in the green infrastructure and broad policy support could be key drivers of this market. By the same token, on the fixed income side the Asian High Yield market could be interesting after a torrid year. Total returns have been negative (according to the JP Morgan JACI Corporate Diversified High Yield index) and the current yield is 7.7%. Yields that high in the past have generally meant decent total returns over the subsequent six months. Of course, it’s highly leveraged credit so selection is important in a market that has seen lots of bonds in distress recently. But there is a good chance the market will re-price to better levels.

It’s Carrick you know

Well the inevitable happened and Manchester United now have their sixth manager since Sir Alex Ferguson retired. I hope Michael Carrick can bring about the decisiveness he showed in the game against Villareal to upcoming Premier League games. The quality of the United players has never been in doubt but there have been issues with organisation and tactics, which have resulted in performances lacking cohesion and ambition. A team with Rashford, Ronaldo and Sancho in the attack should be doing better than eighth in the league table. More clean sheets and attacking pace please!

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.