What comes after the e-commerce boom?

Key points:

- E-commerce boomed during the pandemic and has continued to grow at rates two to three times faster than before the onset of COVID-19

- Though recent months have seen a slowdown in e-commerce growth, sectors such as health care, hospitality, and some retail categories have showed endurance

- Supported by strong demographic trends, the digital economy and e-commerce could bring an array of potential investment opportunities in the long run

The pandemic has affected countless aspects of our lives, including e-commerce. Online shopping boomed during the pandemic, but what’s next?

As our world has trended increasingly digital in recent decades, so too has consumer spending.

To be sure, we’ve come a long way from the introduction of the Boston Computer Exchange in 1982 and the early days of Book Stacks Unlimited a decade later – e-commerce today is widespread, with shoppers now spending trillions of dollars each year online.

While e-commerce blossomed for decades leading up to COVID-19, the sector boomed during the global pandemic – accelerating forward at an altogether different pace. When people stayed in the safety of their homes, e-commerce exploded.

Now that we’re through the worst of the pandemic, the question remains: Will e-commerce continue to soar or taper off?

E-commerce in a pre-and post-pandemic world

E-commerce, in the form that we know it today, burst onto the scene long ago – Amazon opened their virtual doors for business in 1995 – cementing its here-to-stay presence long before the global pandemic. Between 2015 and 2019, e-commerce’s share of all retail sales in the United States rose by an average of 1.4% year-over-year,

Why? Because e-commerce at its best produces a win-win outcome for consumers and retailers alike. Shoppers appreciate the ease of online marketplaces and benefit from being able to search for goods in one place – all from the comfort of their homes and whenever most convenient for them, even outside standard business hours. Businesses, meanwhile, often leverage e-commerce to expand into foreign markets, reduce their B2B sales cycles, collect customer data insights, scale up, and save money.

So while e-commerce announced itself before the COVID-19 outbreak, it was no surprise to see the sector soar to even greater heights thereafter. As many brick-and-mortar retail stores closed their doors in 2020, more people turned to the internet for shopping. Large retailers such as Target, Walmart, and Amazon grew even more popular throughout the early days of the pandemic, emerging as go-to, one-stop-shops for customers to conveniently purchase books, office chairs, and everything in between.

Large, mostly online retailers became uniquely positioned to meet the bulk of their customers’ needs. Compared to smaller retailers that faced more limited resources, the Walmarts of the world proved more effective at navigating supply chain chaos, sidestepping shipping issues, and overcoming inventory shortages.

Against this backdrop, e-commerce’s year-over-year growth more than tripled during the pandemic, jumping from 1.4% to 4.6% in 2020.

That being said, e-commerce’s more recent trend line has painted a different picture.

In fact, in recent months we’ve seen a slowdown in e-commerce growth compared to the initial post-COVID-19 online spending boom. Online sales growth in the US plummeted from 54.4% to 15.4%

During this general cool-down period of online spending, we should note the significant variation across industries. E-commerce growth has notably continued to endure in sectors such as health care, hospitality, and some retail categories – including electronics, clothing, and department stores.

Furthermore, in Q3 2022, overall e-commerce growth rebounded from 7.3% to 10.8% and expanded by roughly $250bn in Q3 2022, thanks in part to Amazon moving its Prime Day sales from June to July.

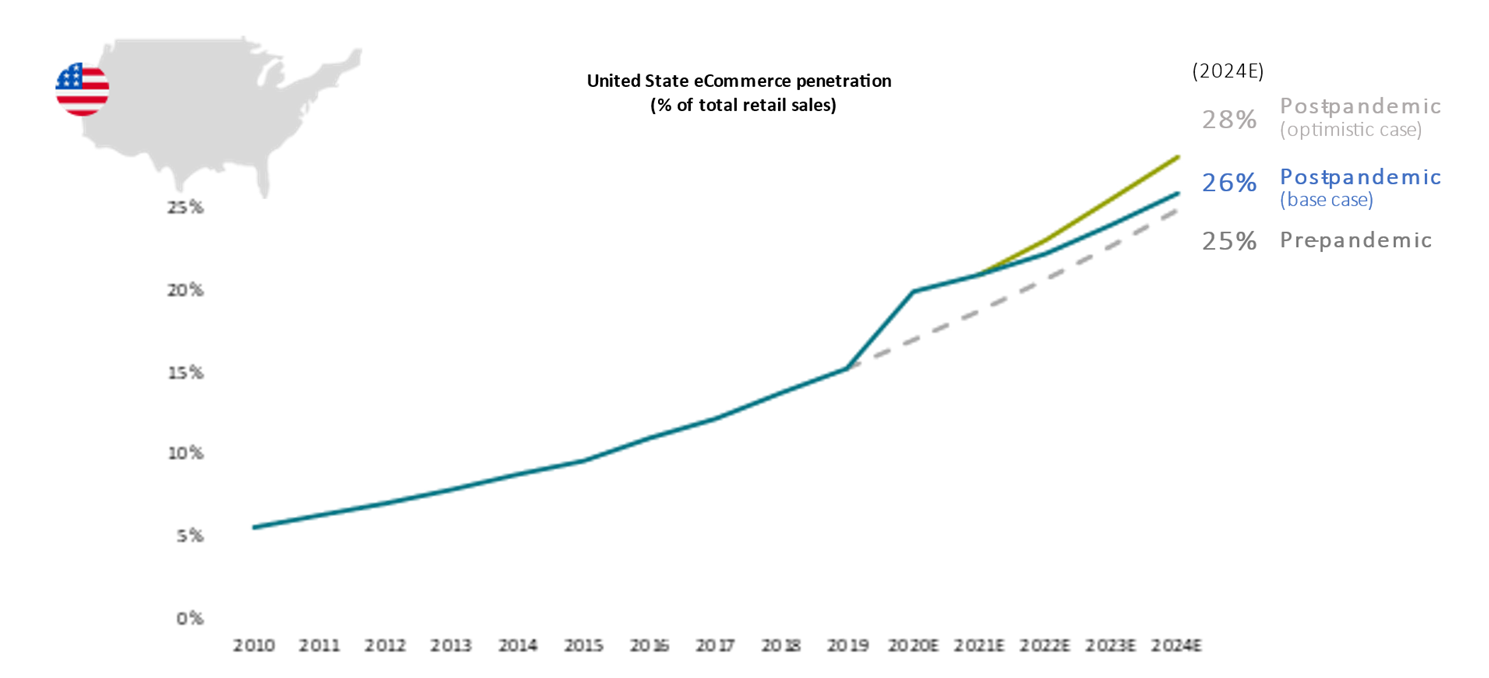

Moving forward, we expect to see e-commerce growth and penetration intensify in the near future. Experts project US e-commerce penetration will account for between 26% (base case) to 28% (optimistic case) of total retail sales by 2024 – a notable uptick from our pre-pandemic estimate of 25% (see chart 1 below).

E-commerce penetration in a post-pandemic world (US)

Source: AXA IM, US Census Bureau, Euromonitor, Prologis Research forecast, August 2022.

E-commerce and the digital economy

Responsible investors that share an appetite for sustainable e-commerce might consider zeroing in on opportunities within the digital economy. In a nutshell, the digital economy refers to how digital transformations have redefined traditional economic activities like consumer spending and B2B.

The advent and adoption of myriad technologies, as well as the influence of a younger, more tech-savvy generation, has brought the digital economy into clearer focus for investors. Thanks to the Internet, the World Wide Web, secure payment gateways and processors, and other technologies, shopping at brick-and-mortar stores is no longer consumers’ only option.

At its core, the digital economy is about driving meaningful online connections between people, devices, data, and organisations or businesses – e-commerce simply represents one of the most recognisable and widely used facets of the digital economy today.

As the digital economy continues to morph into an essential part of today’s world, investors are taking notice – with good reason. Supported by two powerful long-term drivers – evolving demographics and technologies, namely – the digital economy may present exciting opportunities for investors keeping an eye on the long term.

After all, customer profiles and consumer demographics are evolving. Younger, tech-trained generations will increasingly matriculate into the workforce and attain greater spending power. When they do, a higher percentage of their spending figures to occur via online channels. By investing in the digital economy and e-commerce now given these long-term demographic trends, investors stand to reap potentially significant rewards down the line.

In addition, technological advances will only further support online retail. Mobile phones have become powerful, while broadband networks have levelled up – now smarter and more readily available – making online shopping more seamless and accessible. A notable correlation further underscores our optimism: As payment methods and security systems continue to improve, consumer confidence in online payment channels increases – a trend that may hold steady.

The next phases of e-commerce

As we move into 2023 and beyond, investors are turning their attention to what’s next for e-commerce.

Will we see e-commerce growth return to the same heights it peaked at during the height of the pandemic? Though these prior peaks are unlikely, we believe e-commerce volumes are likely to continue to grow for years to come.

On the one hand, given the circumstances surrounding the global pandemic, recent year-on-year growth comparisons pertaining to e-commerce prove inconclusive. Following prolonged lockdowns that left many consumers without brick-and-mortar options, economies reopened. With some consumers returning to the joys of physical shopping since then, e-commerce has continued to grow post-pandemic, albeit at a more muted pace.

For a portion of consumers, a return to normalcy has meant a return to once-normal, pre-COVID-19 spending habits.

That is to say: some people prefer to try on clothes before purchasing; some enjoy going to the mall with friends or relatives; and others like to head out to local coffee shops and restaurants. The point here? Some consumers will always enjoy the ability to partake in more social, in-person experiences that the Internet, so far at least, struggles to replicate.

And yet, there is no evidence to suggest that long-term e-commerce growth trends are broken. Some consumers may head back to brick-and-mortar stores for the basic experience of shopping in person but, online shopping offers plenty of attractive features for consumers and is not going away any time soon.

Moving forward, it figures that retailers will likely be prudent to invest in their digital strategies – that is, if they haven’t already got them – and double-down on technologies that can enhance the e-commerce customer experiences.

Given steady, long-term growth drivers – such as shifting demographics and increasing adoption of advanced technologies – investors may take note of pertinent developments and be ready to take advantage of untapped opportunities within the digital economy.

We see potential in opportunities within the digital economy that touch aspects across the e-commerce experience – from fulfilment and logistics to digital advertising, secure payments, and beyond. By focusing on global growth companies that contribute measurably to the digital economy’s overall value chain, investors may find long-term value within both the e-commerce space and digital economy, at large.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2023 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.