ECB update: Cautiously surfing the dovish wave

KEY POINTS

Little doubts of a 25bps rate cut in October

The September flash inflation print highlighted significant downside to ECB’s forecasts unveiled just a few weeks before. Crucially, core inflation came at 2.7% y/y in Q3 24 while ECB’s forecasts revised in September had 2.9% y/y. Given the surprise came from core components, the downside is likely to transpire at least through a few quarters. In our reaction to the print, we thought it was enough for the ECB to decide on 25bps rate cut in October (no rate cut expected previously at that meeting), also since President Lagarde expressed increased confidence in the timely return of inflation to target in her statement at the European Parliament. Such comments were also echoed by historically hawkish ECB board member Isabel Schnabel, while she also highlighted growth headwinds and softening labour demand, making clear the lack of willingness to fight market pricing which had over 90% probability a 25bps rate cut at the next meeting.

Weak domestic demand with little hope of (imminent) significant pick-up

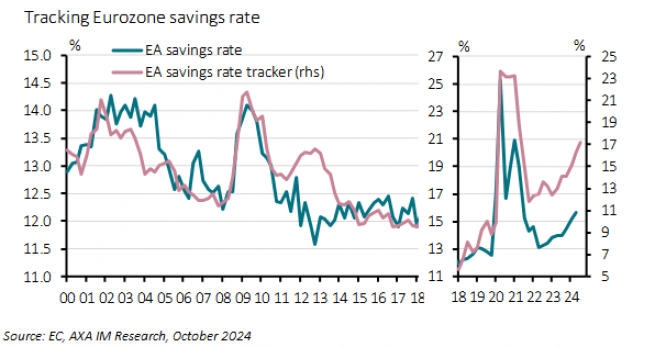

Euro area final domestic demand (aggregated private and public consumption and overall investment) contracted in Q1 and Q2 this year. While this was mainly led by investment, private consumption growth was anaemic, growing by an average 0.1% q/q in H1 24 – and contracting in Q2, despite significant real purchasing power gains. Latest business and consumer confidence surveys are consistent with our view of no imminent material domestic demand pick-up by contrast with ECB’s latest forecasts. We think that softening labour market, significant political uncertainty in Germany and France, and decent real deposit rates are likely to maintain household’s savings rate high, as suggested by our tracker (Exhibit 1), and delay the investment recovery. Downward revisions in these two countries in our latest global macro monthlywere the main driver for lower, still below consensus, euro area 2025 GDP growth forecast at 0.9% (consensus & ECB: 1.3%).

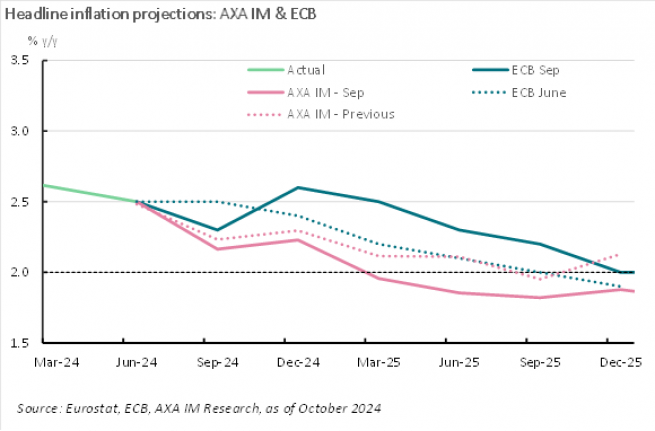

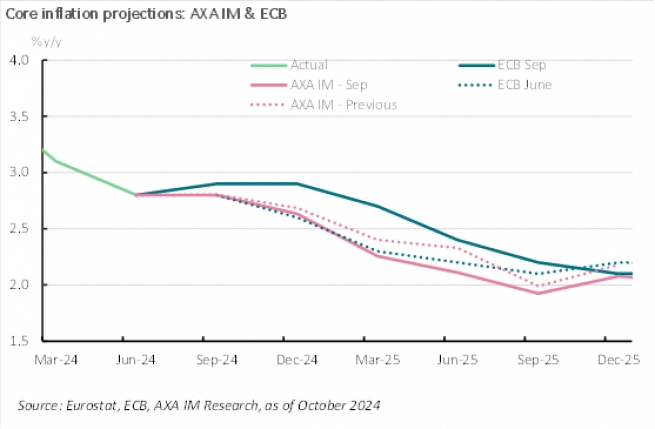

Our latest inflation forecast update shows ECB’s inflation target undershooting for most of 2025

Beyond the abovementioned September inflation print, ECB’s 2025 inflation forecasts look too high. Exhibit 2&3 show similar difference between ours and ECB’s projections for headline and core inflation, implying that oil price assumptions play a likely minor role. Reflecting uninspiring domestic demand prospects, marked by the services-led consumption rotation running out of fuel - we have abated services (and goods) price seasonality. We now forecast headline inflation to come below ECB’s 2% target in the first three quarters of 2025, reaching a low in Q3 25 (1.8% y/y), while core inflation would continue its downtrend without too many humps and bumps.

We now expect back-to-back 25bps depo rate cuts through H1 25 to 2%, with a skew to the downside

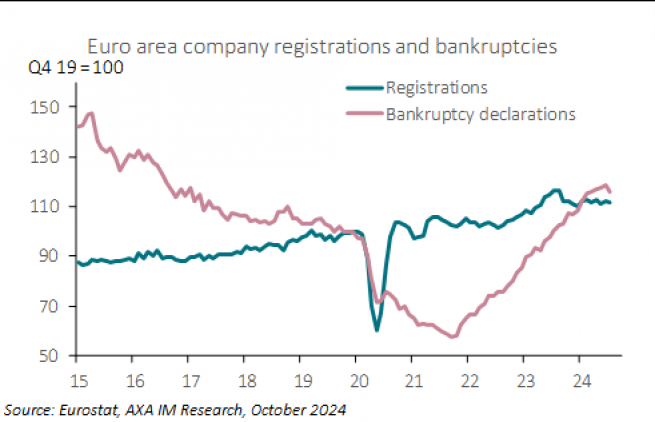

With already minimal deviation of actual inflation to ECB’s target, we think disappointing activity momentum will eventually lead the ECB towards a more forward-leaning policy bias, putting less – though unlikely to fully disappear - weight on its triptic (wage, productivity, unit labour cost) and justifying a step-up in ECB easing its restrictive stance from its quarterly forecast meetings – our expectation since September 2023. While our revised nominal policy rate would be within the vicinity of neutral by-end H1 25, it would be significantly more restrictive than in the previous fifteen years. As such, we cannot rule out the ECB going with a more aggressive easing cycle, either going 50bps in December or continuing for longer its easing cycle depending on data, but also on other central banks’ behaviour. Although euro area inflation sensitivity to euro currency tends to be small, the ECB will have to be mindful of its relative monetary policy stance, cautiously surfing the current overwhelming monetary policy easing narrative across all major advanced economies. Finally, Covid-19 and the 2022 inflation shock and their associated policy response have likely extended a growth cycle that started in mid-2013 that has yet to rollover. Although not an imminent concern, there is a significant net destruction of companies (Exhibit 4) in the euro area while fiscal leeway is very limited to non-existent across member states.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.