Why food waste is a moving target in the climate change fight

Many societies have become relatively comfortable with the idea of just-in-time supply chains that funnel goods to them day in, day out. Less palatable would be just-enough food production and distribution. Individuals have become used to the appearance of plenty – and as supply chain wobbles in 2021 showed, the public spooks easily at the sight of empty supermarket shelves.

Over-production is therefore baked into the system – the alternative is unthinkable – but the implications of that have been inadequately addressed. The data starkly illustrates why that is a huge problem as the world seeks to deliver a transition to net zero emissions over the coming decades.

According to the United Nations Food and Agriculture Organization (FAO) the world wastes about a third of the food it produces for human consumption.

All told, the carbon footprint from wasted food has been estimated at about 3.3 gigatonnes of CO2 equivalent per year – if it were a country, food waste would rank as the world’s third largest emitter, behind only the US and China.

But these aggregate numbers disguise the dispersed and diverse nature of the problem. When we try to get a handle on food waste there are no giant power stations pumping out greenhouse gases (GHGs) for us to latch on to, but millions of moments and transactions at farms, supermarkets, homes and restaurants. And while renewable energy sources may be steadily chipping away at our oil and gas dependency, there is no currently viable alternative to the foodstuffs that keep us all alive, or even the production and distribution networks that put meals on our tables.

Without a perfect replacement system waiting to be rolled out, it is therefore likely that the solutions will be dispersed and diverse too. One 2014 report from the UN’s Food and Agriculture Organization made that clear – the six mitigation methods it chose to highlight ranged from milk coolers in Kenya to improved carrot sorting in Switzerland and stopped in at pig feed in Australia on the way.

Uneven impacts

Food waste happens across the globe, but in sometimes very different ways. In richer nations production has been made steadily more efficient through mechanisation and improved agricultural practices. That means waste tends to occur towards the far end of the supply chain, where excess material is often dumped in landfill and eventually contributes to emissions of methane, a far more destructive GHG (in its unburned form) than carbon dioxide.

If we accept over-production as the only politically plausible reality for an advanced nation (and accept that over-consumption is undesirable for all sorts of healthcare and social reasons) then part of the solution must lie in what we do with food once it has fallen the wrong side of supply/demand dynamics. There are a range of enterprises delivering apps that seek to connect those with spare food with potential consumers. These often operate at a community level, between individuals, but even those that aim to replicate the idea at the level of restaurants and catering businesses struggle to reach the scale which makes them investable for larger market participants.

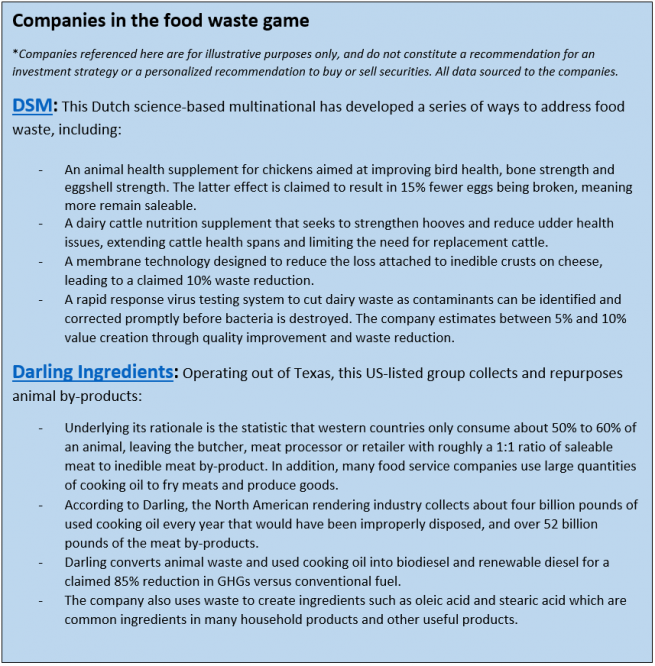

Perhaps more viable are companies trying to produce energy through the collection and distribution of used cooking oil as fuel for major transport firms or taking waste from meat production to create fertilisers.

In the UK – where energy produced through anaerobic digestion increased by close to 60% between 2015 and 2020 – food waste makes up about a third of the material used and crops another third.

On the shelf

Another possible solution that has reached investable scale lies in the innovations that can help to extend the shelf life of products. Fresh foods can spoil easily because they offer an attractive home for microorganisms, but antimicrobial packaging can help address that, as can antimicrobial gases in the air pockets around products like meat or cheese. There may also be a subsidiary effect of reducing the reliance on energy-sapping refrigeration in the logistics chain.

And if we go back to the start of that chain, outside of the investable universe, to the farmers producing the food in the first place, we can see encouraging innovation from something like the US’ Farmers Business Network.

Any discussion around food waste tends to come back full circle. The problems and the solutions are scattered through the value chain, and for investors we believe that should be as encouraging as it is complex. There are potential opportunities everywhere as the world adapts to the net zero future laid out by governments – and as we steadily get to grips with the climate impact of the food system that sustains us all.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the U.K. by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the U.K. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.