Don’t miss the second window of opportunity in fixed income

Key points:

- Investors who missed the boat on bonds at the start of the year have been offered a second chance to capture higher yields by more recent market movements

- We highlight areas including investment grade credit, high yield, inflation and short duration for consideration

- Overall, we believe fixed income markets today offer compelling opportunities to generate potentially attractive returns with downside risk mitigation

At the start of this year there was no shortage of market commentary asserting that bonds are back. For the best part of the previous decade, a record low-yield environment had pushed investors up the risk spectrum and dramatically reduced fixed income’s ability to play either of its expected roles of providing reliable income or as a hedge against riskier assets in the case of a weaker growth outlook. This all changed with the sharp sell-off across bond markets in 2022, that left fixed income yields and valuations at a far more compelling starting point for 2023.

Unsurprisingly, investors piled into bonds over the early weeks of the year, with yields declining strongly over January, leaving some to question whether they had already missed the boat for the ‘year of fixed income’. However, yields have since sold-off sharply once more, offering a second chance to allocate to fixed income at much more attractive valuations.

Against a backdrop of strengthening economic data, inflation has started to moderate but not as quickly as policymakers would hope. Market sentiment has turned more cautious over February as investors weighed the possibility of a delayed recession later this year and, in the meantime, higher for longer interest rates. Even more recently, concerns over the banking sector, while pushing government bonds yields sharply lower, have widened spreads in the investment grade and high yield credit markets as risk premiums on corporate bonds have risen.

AXA IM’s fixed income team expect further volatility ahead, but we believe longer-term the outlook for fixed income has become more positive with better potential to add resilience and diversification to portfolios from a more attractive entry point. The key will be to look across the breadth of the fixed income landscape in search of the best opportunities to navigate such an uncertain environment.

Investment grade credit in a sweet spot

With the economic, inflation and policy outlook still so unclear, we favour higher quality parts of the market, such as investment grade credit in both the US and Europe. We currently see good value in investment grade credit, combined with potential resilience against market uncertainty owing to diversified sources of return coming from both interest rate and credit spread components.

Clearly sentiment in the Banking sector has been tarnished, which will weigh on spreads and risk assets. Although further banking problems cannot be ruled out, recent policy initiatives from the Federal authorities should help contain the risks. We do not see a systemic risk of a run on the entire banking system when deposits would be withdrawn and held in physical cash, as has typified bank runs in the past. The banking system as a whole is well capitalised, there is flexibility to provide broader deposit insurance and policy makers have many tools to use to provide liquidity to markets. In Europe, the risk of potential deposit flight from banks seems less than in the US while bank balance sheets have been more conservatively managed. From a credit point of view, we have a positive view on European Financials but have begun to shift out positive view on US Financials.

More broadly, we expect investment grade credit fundamentals to remain resilient as companies have reported strong balance sheets and high liquidity levels after benefitting from cheap debt refinancing over the past few years. This should limit the extent to which spreads widen if a recession materialises. An unconstrained, flexible approach aimed at optimising total returns across the credit cycle could be particularly interesting in a changeable market environment.

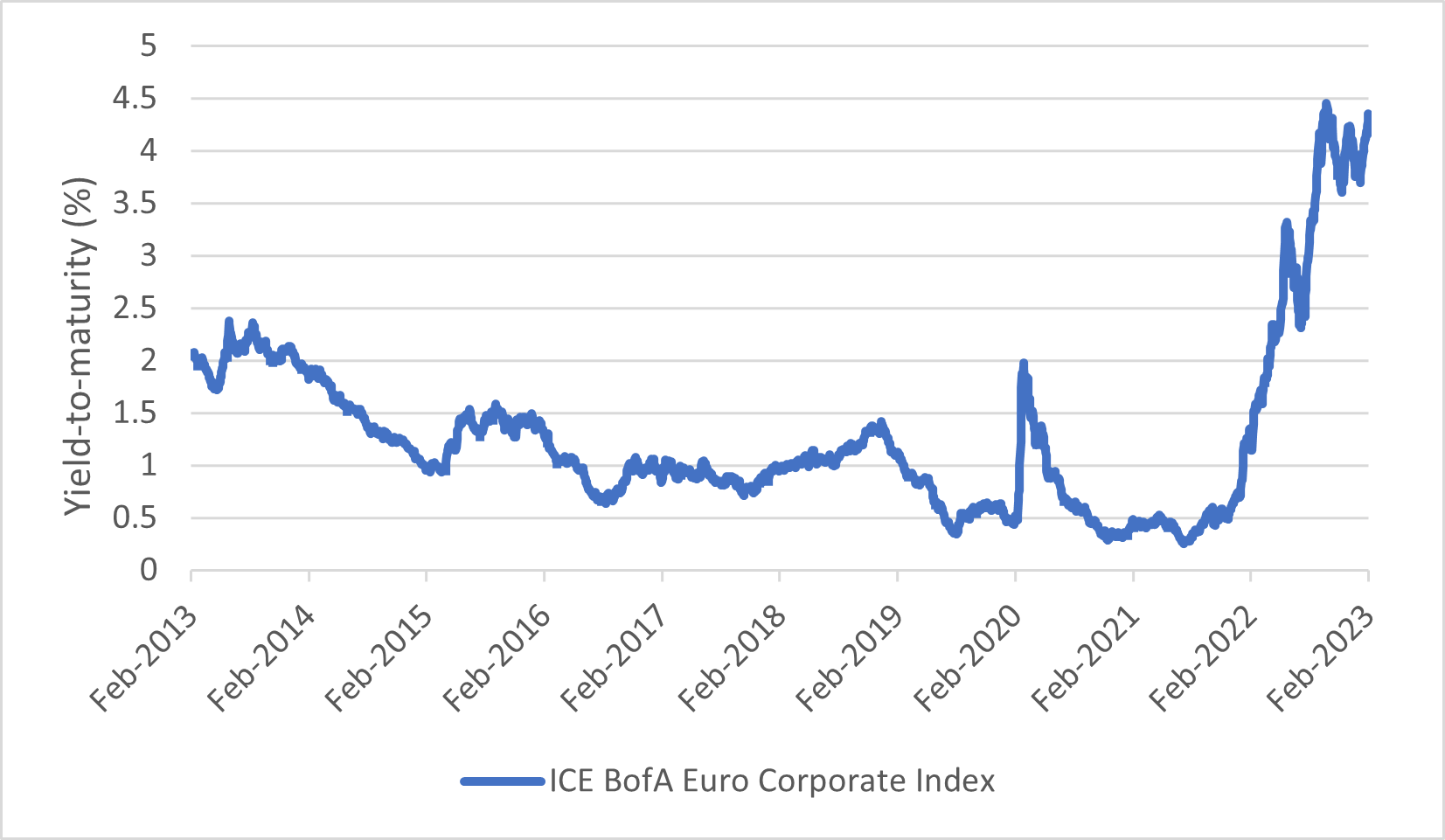

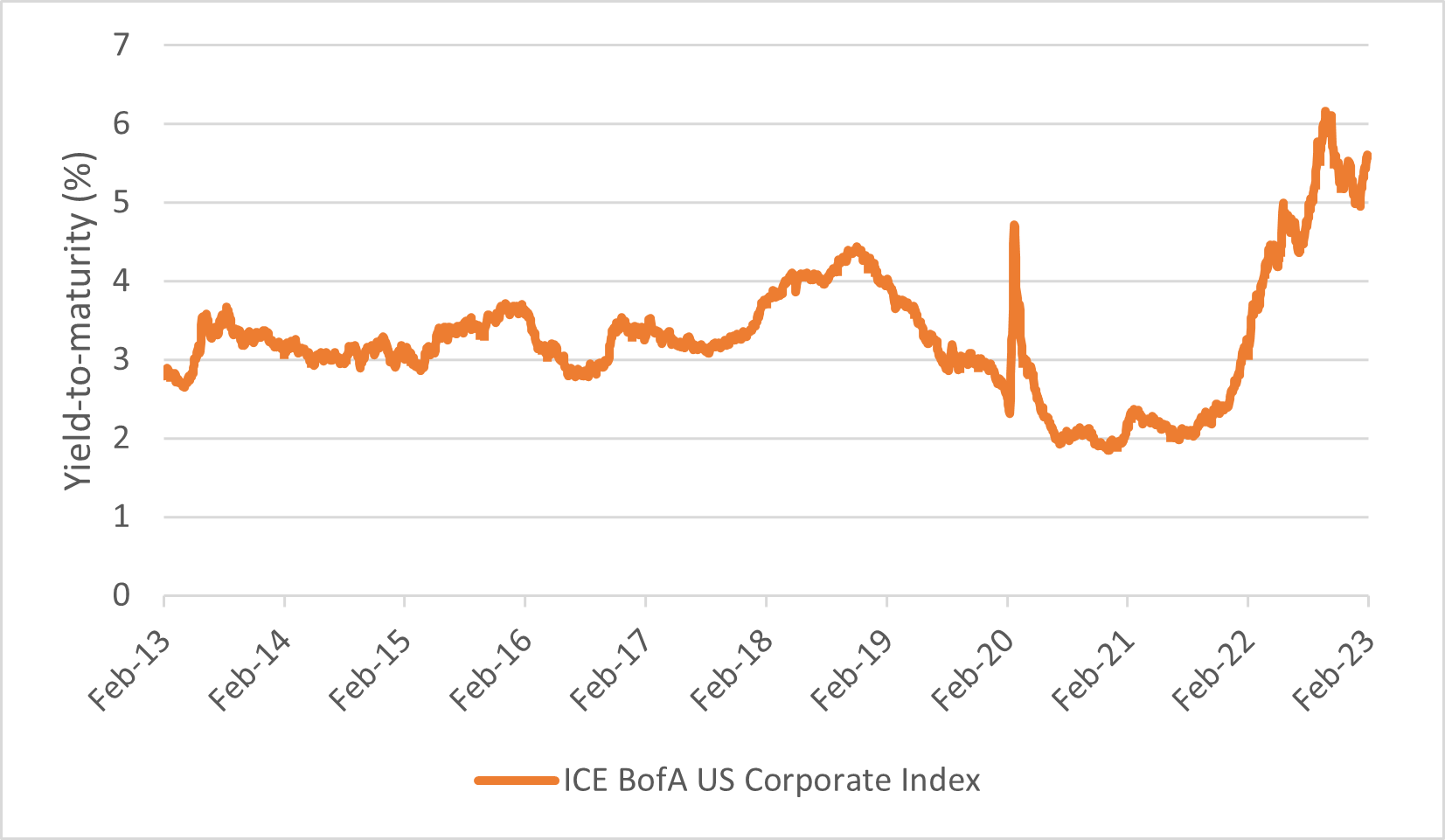

US and Euro credit offer attractive valuations

Source: AXA IM, Bloomberg as of 28/02/2023

The inflation story isn’t over

Headline inflation has fallen but core inflation has remained more persistently elevated. We expect moderation to be slow and the short-term inflation picture is far from clear and remains the key concern for investors. In this context, rather than choosing between inflation-linked and nominal bonds, it could be worth considering a strategy which can flexibly allocate between both.

Selective opportunities in high yield

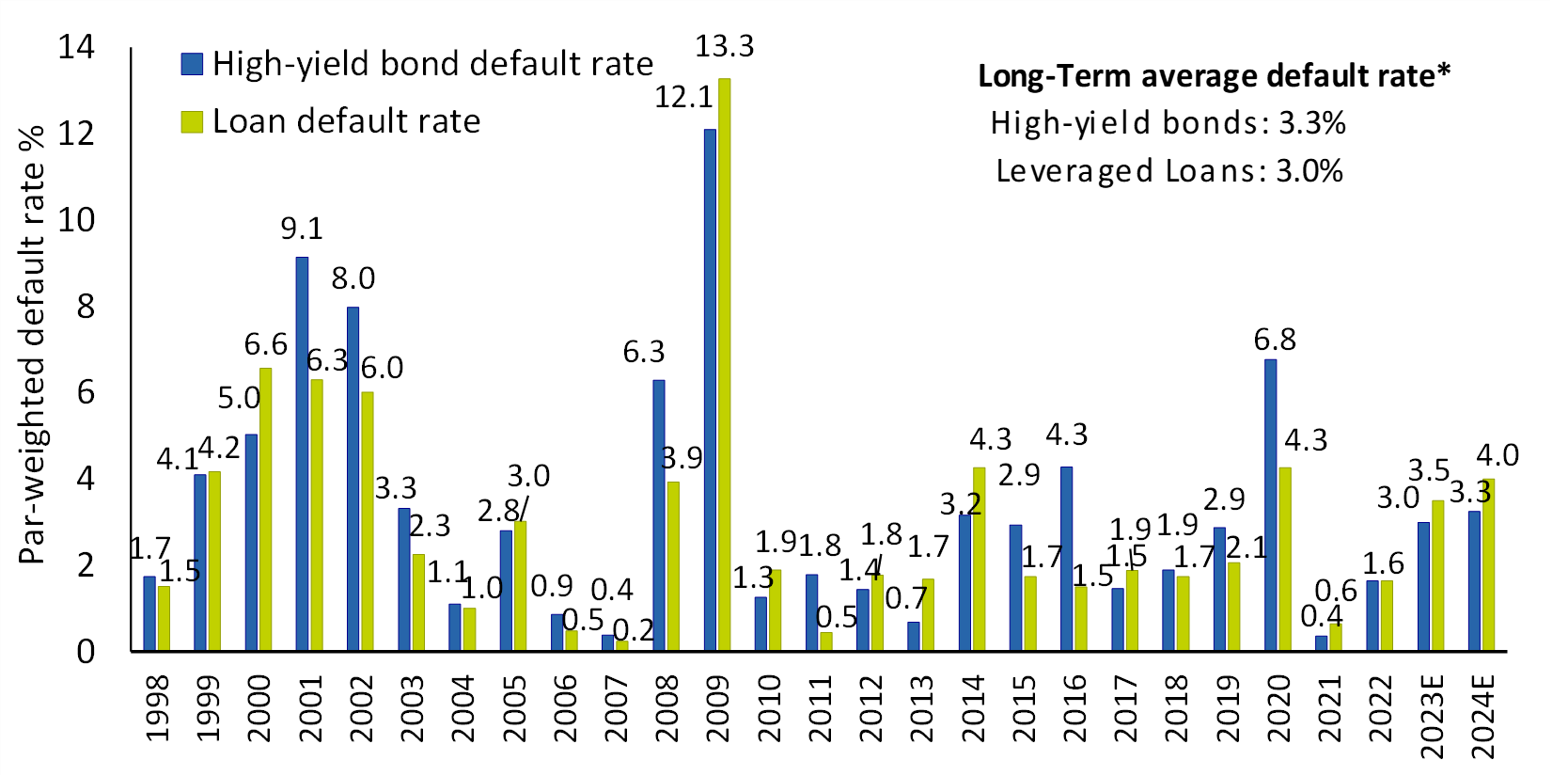

High yield (US, European and Asian) had already delivered strong returns over the start of the year but market weakness in February and March provided another opportunity to allocate to high yield at levels of valuation which appear to well-compensate investors for taking on high yield risk. Current high yield spread levels are indicating a higher default rate than we expect. Defaults are still below historic levels and, in our view, should remain muted, supported by strong fundamentals.

US high yield bond default rates below historic average

Source: J.P. Morgan: Default Monitor March 1, 2023. *High-yield bonds Long-Term default rate since 1997, Leveraged Loans Long-Term default rate since 1998. Due to the subjective aspect of these analyses, the effective evolution of the economic variables and values of the financial markets could be significantly different for the projections which are communicated in this material.

Nonetheless, in an uncertain environment, active management and careful security selection within high yield is vital to benefitting from the yield advantage without overreaching on risk. The same can be said for emerging market debt where very elevated yields are presenting some compelling opportunities but it will be important to be highly selective in weighing potential risk versus reward.

Short duration is tactically attractive

For more cautious investors, short duration approaches offer a potentially good hedge to more volatility around interest rates. Short duration offers the potential to generate superior risk-adjusted returns and currently, the short end of the curve is presenting the opportunity to add attractive carry with mitigated duration risk. Short duration approaches can be used to access any of the above themes through short duration strategies on investment grade credit, high yield or inflation.

Overall, although the recent Banking sector episode is a reminder to always be attentive to macro-financial developments as a potential harbinger of fragilities in the real economy, we believe fixed income markets today offer a diverse selection of opportunities, generate potentially attractive returns and add a source of resilience to portfolios during the uncertain market environment we expect to continue for the remainder of 2023.

Fixed Income

We cover a broad spectrum of fixed income strategies to help investors build diverse portfolios that can be more resilient to economic and market shifts.

Find out moreDisclaimer

This market communication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.