What to do with inflation linked bonds when inflation rolls over

Key points:

- Inflation should slow but remain elevated by historical standards keeping balance of risks tilted to the upside

- Market pricing of future inflation and rates are inconsistent.

- Long positions on inflation linked bonds may offer attractive risk/return opportunities

Disinflation is the name of the game so far this year

Perhaps understandably, disinflation is becoming a buzz word for 2023: in the US, both headline and core consumer price inflation (CPI) have peaked while in the Eurozone, headline CPI seems to have reached a tipping point. Nevertheless, we expect inflation to remain elevated this year and above central banks’ targets. This is because it is likely that monthly inflation will remain high as risks are still tilted to the upside. Just in this first quarter, factors such as the re-opening of China could contribute to higher global energy and commodity prices. Such upside risks may slow the pace of deceleration and mean that income from inflation-linked bonds remains positive.

Even if inflation trends lower in the early part of this year, other upside risks could see an inflationary rebound over the summer. Deglobalization, fiscal spending and the green revolution are among the main factors that could push inflation while the big unknown is whether a recession will be enough to bring inflation down.

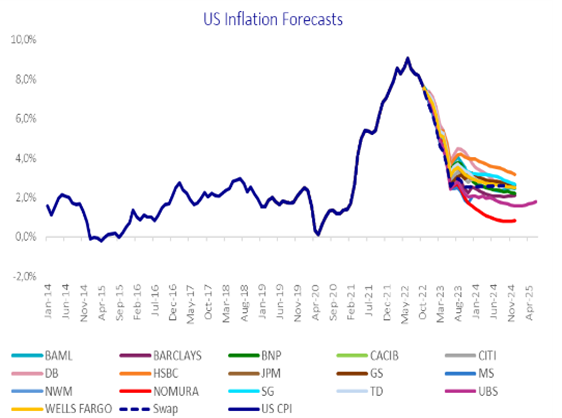

The market currently pricing inflation to be transitory

So, is now the time to take off the duration hedges and hold duration? We believe that it is - at least in the near term. The reason being that there is inconsistency in the major bond market with the market so convinced that there will be disinflation that it currently prices inflation to be “transitory”.

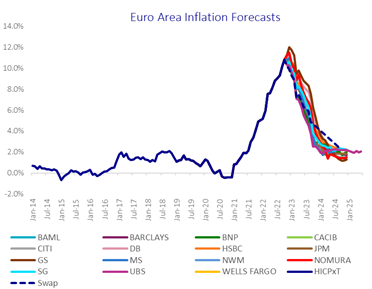

As our December 2022 inflation survey shows, economists’ forecasts show that inflation is expected to be broadly back to target at the end of 2023.

Source: AXA IM, primary dealers. For illustrative purposes only

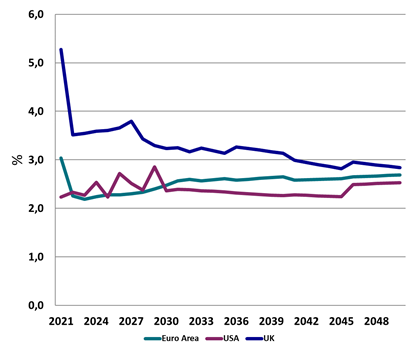

It is then expected to stay close to target for the next 30 years:

Source: AXA IM, Bloomberg as at 31/12/2022. For illustrative purposes only. There is no guarantee forecasts made will come to pass

Market pricing of inflation looks unreasonable

We think that the market is complacent in its pricing of future inflation especially considering that inflation has proven to be more persistent than expected and has become more broad-based. Therefore, this market pricing of inflation looks unrealistic. Inflation has proved to be highly volatile and at times higher or lower than central banks targets, however markets expecting inflation close to targets for the next 30 years looks ambitious. Therefore, inflation could be higher or lower but reaching 2% and staying there is very unlikely. While the recent fall in energy prices may create a near-term downside risk, particularly for short duration which is more sensitive to oil than to interest rate movements, the medium-term risks are to the upside

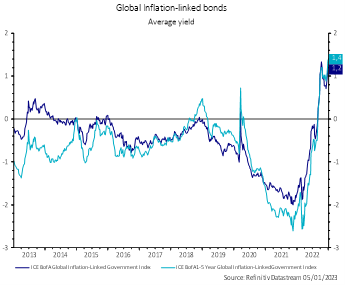

At the same time that inflation is priced to be back to target, the market is pricing the most restrictive monetary policy since the euro financial crisis. We use real yields as an indication of how tight monetary policy is expected to be with positive real yields signaling a tight monetary policy. Real yields were negative for the past 10 years, but as the chart below demonstrates, they are now at their highest level in more than a decade.

Source: AXA IM, Refinitiv Datasteam as at 05/01/2023

We believe that inflation & rates markets are sending inconsistent messages

So, on the one hand the inflation market signals that inflation should normalise but, on the other hand, rates markets signal tight monetary policies. This may be the greatest inconsistency of 2023.

Position on the long side to potentially take advantage of this situation

To navigate these uncertain markets, we believe investors should look to position their inflation portfolios on the long side to take advantage of this situation. This is because long duration positions on inflation linked bonds have a dual exposure to inflation and rates. As things stand, either rates are too high or inflation priced into the market is too low. Either way, one has to give. We believe that buying inflation linked bonds and keeping the duration exposure may offer good risk / return opportunities for 2023.

Inflation

Inflation can erode the real returns of investments however tools like inflation-linked bonds could help investors mitigate the effects of inflation on their portfolio.

Find out moreDisclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.