Why consider inflation-linked bonds in a stabilising rates environment

Key points:

- While rates are expected to stabilise, inflation remains historically high and above central banks’ 2% target.

- Why investors may want to re-evaluate their inflation-linked bond allocation.

- What inflation-linked bonds offer in this market environment.

Softer economic data and hawkish messages from central banks have led markets to expect a pause in rate hikes. If rates are stabilising, what does this mean for the inflation-linked bond asset class?

Investor behaviour often means that inflation-linked bonds see strong inflows as inflation takes off and then sharp outflows when nearing the peak regardless of what the inflation level is. This current inflationary cycle has been no different and investors began moving away from inflation-linked bonds towards the end of 2022 as the headline inflation peak was anticipated. This trend continues today. The challenge for investors, however, is that inflation is still high even by historic standards. Despite the lower-than-expected outcomes for inflation in October, core inflation remains elevated. Alongside this, any measure is still above central banks’ 2% target with growth data not yet weak enough to realistically expect inflation to fall back to this target level.

Inflation is sticky and we expect it may be a problem for the next decade. Factors that might see inflation remaining sticky such as the green revolution, the recent “onshoring” trend and budget deficit concerns mean inflation levels could remain volatile for the foreseeable future.

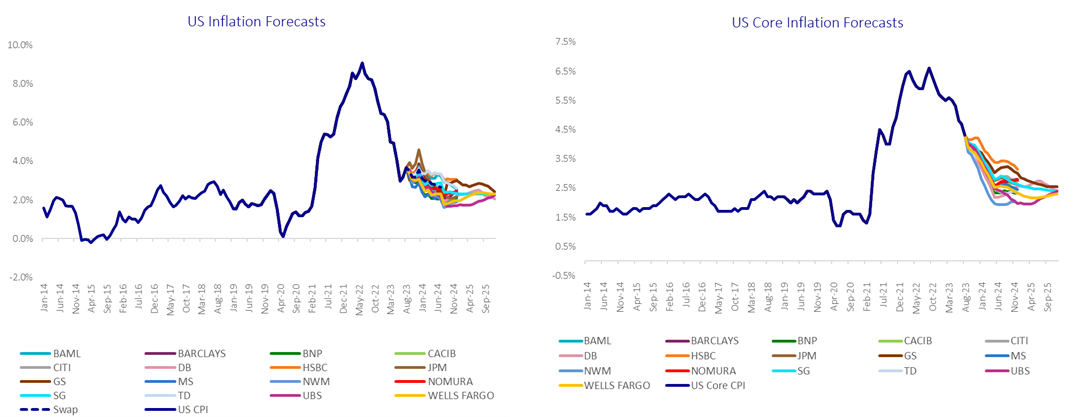

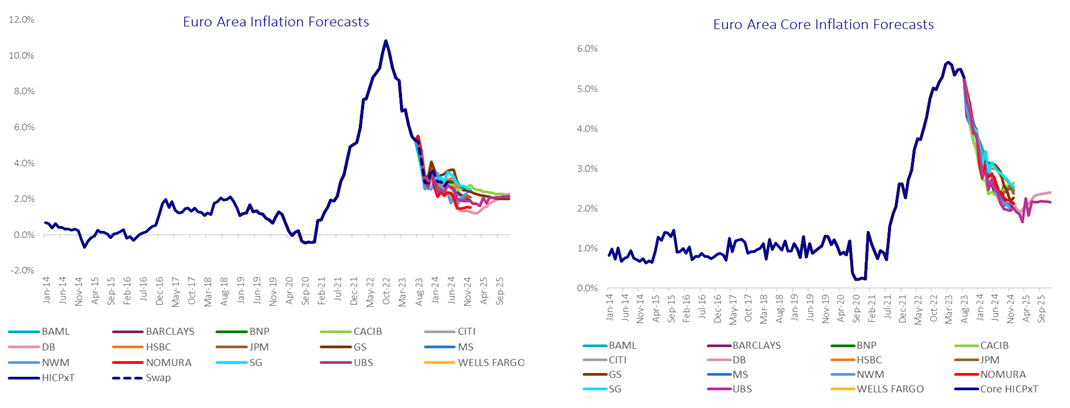

Nevertheless, as the charts below shows, economists are still projecting a return to around the 2% target levels by the end of 2024 and inflation to remain above pre-covid levels particularly in the Euro Area

Source: AXA, Bloomberg as of September 2023

Added to this, market-based inflation expectations for next year are very close to 2%, well below the economists’ and central banks’ forecasts. As the chart below shows, long term inflation breakevens suggest that the market is pricing future inflation at similar levels to those seen between 2010 and 2013.

USD, GBP and EUR Swap rates

Source: AXA IM, Bloomberg as at 17th November 2023

Market conditions offering opportunities

The yield curve remains inverted and this has, historically, been followed by a yield rally: market signals are making a stronger case for duration than we’ve seen for a while. Considering this expectation of a duration rally once core inflation turns, adding duration as core inflation rolls over may be an interesting opportunity.

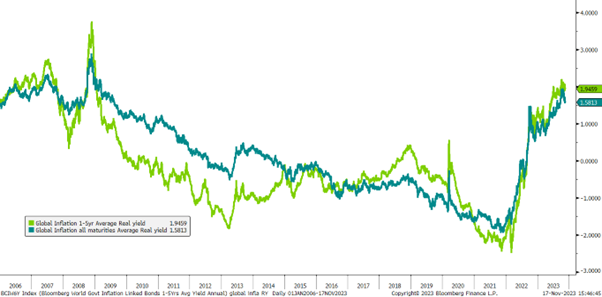

When inflation moderates, inflation breakevens tend to go down as it has been the case in the past month. This combination of elevated levels of real yields and moderate level of breakevens is where we see opportunities. Inflation-linked bonds’ average real yields are currently at their highest average level since 2009-2010 but they are positive suggesting that investors can lock-in an above inflation income.

Global Inflation Average Real Yields

Source: AXA IM, Bloomberg as of 17 November 2023

We believe that the combination of this with the market complacency towards future inflation risks suggests that inflation-linked bond investors may be able to lock-in positive real yields at their highest level post Lehman while getting exposure to inflation breakevens, (effectively a form of insurance premium against future inflation) at historically attractive levels.

With inflation likely to be volatile for the foreseeable future, inflation-linked bonds may be a useful tool for investors because they should provide resilience against sticky inflation. As all inflation-linked bonds cashflows are also indexed to inflation, and their issuers are often highly rated sovereigns, investing in inflation-linked bonds may be used as part of an investor’s capital preservation strategy.

Explore Fixed Income opportunities

We cover a broad spectrum of fixed income strategies to help investors build diverse portfolios that can be more resilient to economic and market shifts.

Learn moreDisclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.