Japan - Once the pandemic is over, Japan may leverage on some tailwinds

Key points

- Japan hasn’t been as badly exposed to COVID-19 as other countries and significant support from the government and the Bank of Japan make it more resilient. Some restrictions may return in the coming weeks, but it should be less strict than in April

- Private consumption is crucial for the outlook, a high saving rate, job market resilience and large demand stimulus should underpin this outlook

- After a -5.5% contraction in 2020, we believe GDP should rebound by +3% in 2021 and +2% in 2021

Pandemic management remains crucial

The short-term outlook remains constrained by the evolution of the pandemic. Japan has been resilient so far and currently only 15% of intensive care unit is occupied nationwide. The number of new cases is rising but we believe Japan will be able to cope with a resurgence of the pandemic without having to impose strict restrictions. Large and coordinated support from the government and the Bank of Japan (BoJ) has been, and will remain, crucial

Private consumption is likely to drive Japan’s recovery. Last year’s sales tax hike and the pandemic have distorted consumer behaviour, but some tailwinds may facilitate the rebound. Income has been largely preserved thanks to various fiscal support from the Employment Adjustment Subsidy Programme as well as cash handouts to households and SMEs

In terms of investment, the outlook is more mixed. On one side, the capital stock has not been destroyed and production – related investments should be muted until demand accelerates substantially. On the other, Japan is likely to accelerate into digitalisation with a ¥15tn plan included in the 1st supplementary budget, while 2021 budget should contain tax incentives. In addition, PM Suga would like to endow Japan with a plan to reach carbon neutrality by 2050. It is too soon for concrete figures, but the country may see large stimulus in sectors such as energy, transport and housing. On trade, we also expect a gradual recovery over the coming quarters with the global economy likely shifting into an expansionary phase. The greatest risk could be another virus-related supply-chain disruption in the US.

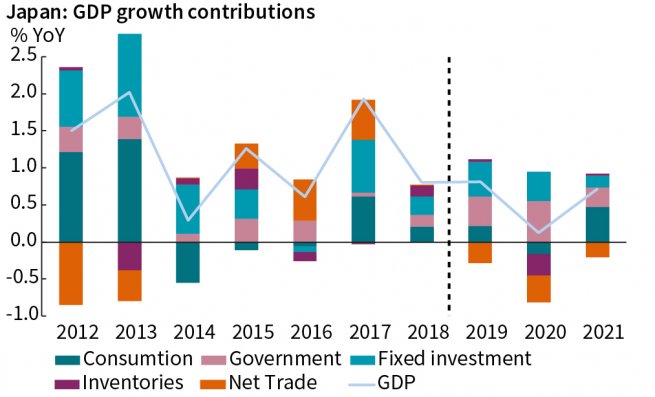

Overall, we expect GDP will rebound by 3% in 2021 and 2% in 2022 (Exhibit 1). Despite positive headlines, GDP isn’t expected to return to its pre-crisis level before Q2 2022. Assuming Japan’s potential growth continues at around 0.5%, this would be 0.6ppt below potential at that time.

Exhibit 1: GDP growth and contributions

Falling inflation could increase BoJ discomfort

In the short term, CPI inflation should weaken further, depressed by a sharp decrease in the output gap and the impact of some measures such as the “Go to” campaign, and a likely lowering of mobile phone charges. Consequently, CPI should decline to -0.2% in 2021 and only rise to 0.1% in 2022.

In this context, the BoJ will face additional calls for more accommodative policy. There is still leeway on its special programme to support corporate financing and we believe that this should be extended until Q3 2021, as long as the demand exists. In parallel, the BoJ will continue to flexibly adjust its JGB purchases, facilitating the additional issuance by the government. The BoJ will be keen to avoid taking rates deeper into negative territory, considering the possibility of further stress on the financial system. Finally, if the yen appreciates beyond the implicit ¥100/USD threshold, the BoJ may face a difficult decision.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.