Multi-Asset Investments Views: Take me higher

KEY POINTS

Markets successfully navigated both macroeconomic and geopolitical hurdles this summer and we believe they have the potential to continue to push higher. The ongoing absence of any renewed bouts of angst, and hence a pull-back in prices or risk appetite, is unusual, with more than 100 days without a retracement of 2% on the S&P 500. We believe the explanation lies in discretionary investor positioning: while systematic strategies are generally aggressively positioned relative to history, the discretionary part of the professional market lightened up on risk going into the summer. That has left a balance of demand, with investors fearing they would miss out on the ongoing rally, which in turn has driven it to the current self-fulfilling outcome.

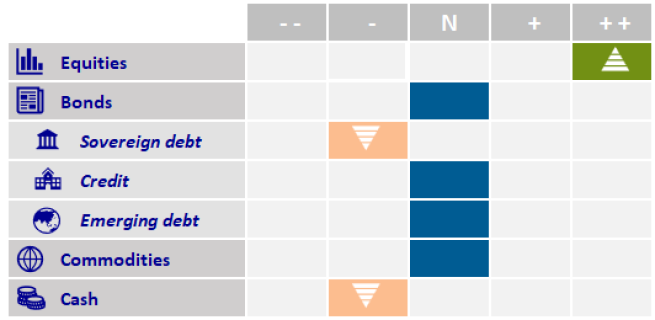

Given the combination of Federal Reserve (Fed) projections indicating rate cuts into year-end, buoyant US activity and hopes for renewed stimulus in China, we believe the rally can extend further. We continue to hold a significant overweight in equities.

The Fed’s September meeting was a masterclass in both expectation management and integrity reassurance. Despite continued pressure from the US administration via both the media and the courts, Fed Chair Jerome Powell delivered the cuts the market had priced in since the dramatic downside revisions to jobs data. Yet, on the other hand, the most vocal doves – other than newly appointed Governor Stephen Miran - sided with Powell and voted for a 25-basis-point cut rather than dissenting in favour of a greater reduction. This comforted those investors who had begun to question the integrity of the Fed’s independence.

While inflation remains sticky at around 3% and growth buoyant, with the latest GDP growth figures at more than 3% (annualised), delivering both parts of the Fed’s dual mandate of inflation and unemployment will remain challenging. US dollar weakness has persisted, due largely to the reduction of the interest rate gap, especially with Europe. However, we continue to be mindful of any further attacks on the Fed’s independence and focus on the US Supreme Court decision on Fed Governor Lisa Cook’s attempted dismissal. We remain sellers of US dollars (with a $1.20-to-€1 target) and absent from US duration, cautious of potential further curve steepening.

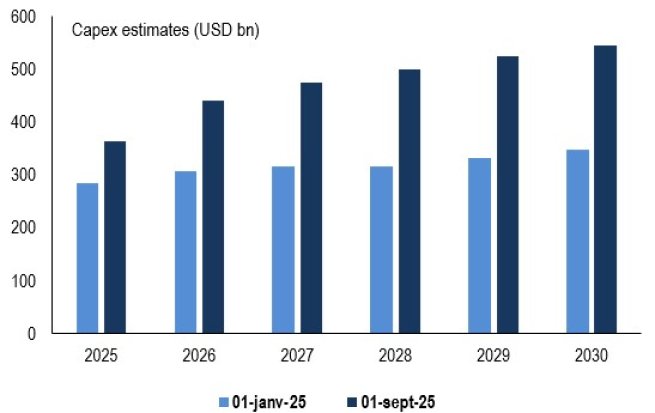

Our equity risk appetite is essentially focused on the case for greater US equity performance, driven by the enormous level of infrastructure investment to accommodate the artificial intelligence boom (see chart below). Still, we remain eager to broaden our risk to other geographical areas and/or sectors. We see potential in the recent strong rally in Chinese equity markets, driven by the expectation of another round of stimulus following poor macroeconomic data. Domestic retail investors are also providing increasingly important inflows. Where appropriate, our preference is for China technology stocks, which benefit from strong earnings growth and a large valuation advantage compared to their US peers.

Meanwhile, the tone adopted by European Central Bank President Christine Lagarde has once again veered to the hawkish side, leaving investors now pricing less than one further interest rate cut. We find this stoicism somewhat misplaced and cannot square that circle. Germany - the Eurozone’s largest economy - has been going through two years of near recession, while France – the bloc’s second-largest - is sluggish, though there is better growth in Southern Europe. We believe a rate cut can be priced back in, with deflationary forces still weighing on the region through the strong currency, weak energy prices and large-scale redirecting of Chinese exports from the US to Europe. With such asymmetry, we hold on to our long position in short-dated German bonds.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.