Multi-Asset Investments Views: Where are we now?

KEY POINTS

After six months of US-policy-driven volatility - including the third-highest stress spike in modern history, only surpassed by the events of COVID-19 and the 2008 global financial crisis - we enter the second half of 2025 with fundamentals and valuations close to where they were in January.

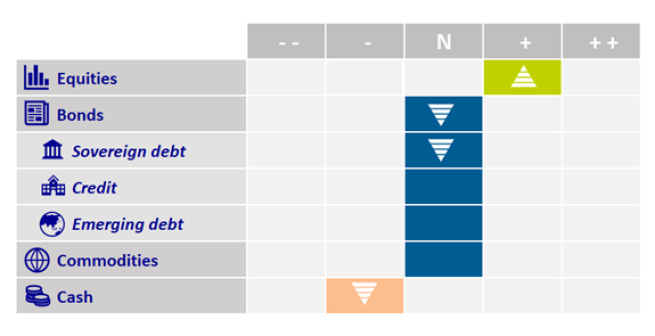

Whether this is to be judged to be complacent, or plain uncomfortable, it is a relief to have such an elevated degree of excitement behind us and currently we are modestly overweight in terms of risk appetite.

On the macroeconomic front, the worrying gap between free-falling, forward-looking soft data (consumer confidence and business surveys) and resilient but backward-looking hard data (especially retail sales and trade flows), partly narrowed in a positive fashion. This gap usually signals trouble ahead and is therefore one of the back-tested indicators we factor into our tactical risk appetite framework. At one end of this gap, hard data remained relatively steady and has not weakened to the downside (at least not yet, would add the pessimist). As the Atlanta Fed’s GDP growth tracker in real-time summarises, at +3.4% annualised for the second quarter (Q2) of 2025 (as of 18 June) and significantly above US potential growth, the economic contraction in Q1 2025 no longer seems to have been the start of a softer growth patch.

The US labour market is also resilient. Although job creations are, and will continue, slowing in our view, the collapse in immigration considerably reduced the number of new jobs needed to stabilise the prevailing US unemployment rate at 4.2% which is at the same level as almost a year ago. Finally, US inflation news flow is also benign, coming in at, or even below, economists’ expectations. Federal Reserve Chair Jerome Powell could today readily repeat his statement from May 2024: “I don't see the stag or the flation”.

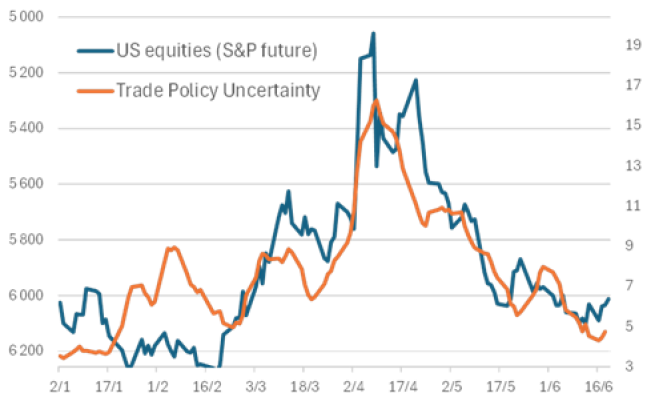

At the other end of the soft/hard data gap, the former has modestly bounced higher - for example the NFIB optimism survey of US small and medium-sized companies is rising, including on hiring intentions in the coming months. This improvement in sentiment may simply reflect the sigh of relief accompanying US President Donald Trump’s speedy back-pedalling on tariffs, which takes the worst-case scenario off the table – both in the short and long run, in our view. With US Treasury Secretary Scott Bessent (a tariff dove) surpassing in influence chief trade adviser Peter Navarro and US Secretary of Commerce Howard Lutnick, (some of the tariff hawks), the peak of US trade policy uncertainty is likely behind us. The US administration’s change in attitude (see chart below) is in no small part guided by China’s weaponisation of its rare earth reserves, a much more credible and damaging strategic threat than further selling of its holdings in US Treasury bonds.

Despite this relatively benign – if not favourable – fundamental background, the speed and magnitude of the stock market rebound is a reasonable hurdle to restrain our overweight in risky assets. That is the signal provided by our Equity Risk Premium measure (ERP), which merely states that equity valuations are back to expensive, especially compared to the not-so-risk-free US Treasury market. This cautionary message is reinforced by the momentum in ERP (the speed of the rebound) which also weighs on our tactical risk appetite.

What then keeps us modestly overweight in portfolio risk allocation? US retail investors “bought the dip” (or the drawdown as we would refer to an 18% peak-to-trough drop), as they have done repeatedly since the lifting of the COVID-19 lockdowns. They are, in line with the hedge fund community, already back to or close to their historical maximum exposure to equities.

Conversely, a significant part of systematic strategies lagged this V-shaped rally, hampered in their re-risking by the elevated level of ‘recent past’ volatility. Positioning proxies for such rule-based strategies indicate that they are on average only back to neutral in terms of equity risk. Bar a new significant shock in volatility (which Middle East tensions have not led to so far) and with the extreme spike in volatility progressively exiting these backward-looking time frames, we expect systematic strategies to gravitate back towards their maximum levels of equity exposure that prevailed at the start of April. This should potentially offer a strong technical support of flows to equity markets.

Within equities, we took our regional allocation back to neutral. We are mindful of the European stock market outperformance versus the US, with the price action and narrative becoming too consensual and therefore overcrowded. We maintain our preference for quality large caps over small caps, especially in the US stock market, which serves to reinforce the defensive tilt of our portfolios. We are concerned that small caps are more sensitive to rising interest rates and more vulnerable to a potential cyclical fade as tariff frontloading is mechanically reversed. We monitor investor positioning and find that recent inflows into US small caps make for an unattractive risk-return profile going forward.

Within fixed income, we generally tend to prefer Bunds to Treasuries, in part because of the US fiscal outlook with supply set to remain elevated, but also when factoring in the deteriorating attractiveness of US debt and US dollar-denominated assets for non-US investors.

Mindful of the rising trend in US, but also importantly in Japanese interest rates, pulling all global yields higher, we trimmed the long-term interest-rate sensitivity of our portfolios back to neutral and favour short-dated German bonds to express our view that recent European Central Bank hawkishness will be short-lived.

Altogether, after an extremely volatile first half of the year, we remain confident that diversified multi-asset portfolios can potentially deliver appealing risk-adjusted returns in the second part of 2025. We wish you an amazing summer and hope you get to enjoy a well-deserved break.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

Image source: Getty Images

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.