Take Two: ECB raises rates and cuts growth forecast; US inflation rises

What do you need to know?

The European Central Bank raised its benchmark interest rate by 25 basis points to 2.25%, its first hike since 2023. Eurozone inflation climbed to 3.2% in May, from 3.0% in April, due to the Middle East conflict. The ECB has revised up its inflation expectations and lowered its growth forecasts, reflecting “a more pronounced impact of the war”. It now expects inflation to average 3.0% in 2026 and 2.3% in 2027, compared to its March forecast of 2.6% and 2.0% respectively. The ECB also now expects eurozone economic growth to average 0.8% this year and 1.2% next year, revised down from 0.9% and 1.3%.

Around the world

US annual inflation rose to 4.2% in May, up from 3.8% in April - the fastest pace in three years as the Middle East crisis drove energy costs higher. Core inflation, excluding energy and food, edged up to 2.9% in May after a 2.8% rise the month before. The US Federal Reserve is still expected to keep interest rates on hold when it meets this week but market expectations of a rate hike later this year have increased. Elsewhere, China annual inflation rose 1.2% in May, in line with April’s increase.

Figure in focus: 1.8%

Japan’s economy expanded by less than initially estimated in the first quarter of 2026, but still outpaced Q4’s growth, revised figures show. On an annualised basis, GDP rose 1.8%; lower than the initial official estimate of 2.1%, but up from Q4’s downwardly revised 0.7%. The adjustment to Q1 growth reflected lower capital expenditure as businesses scaled back investments amid geopolitical and economic uncertainty. The Bank of Japan is widely expected to raise interest rates by 25 basis points to 1% when it meets this week.

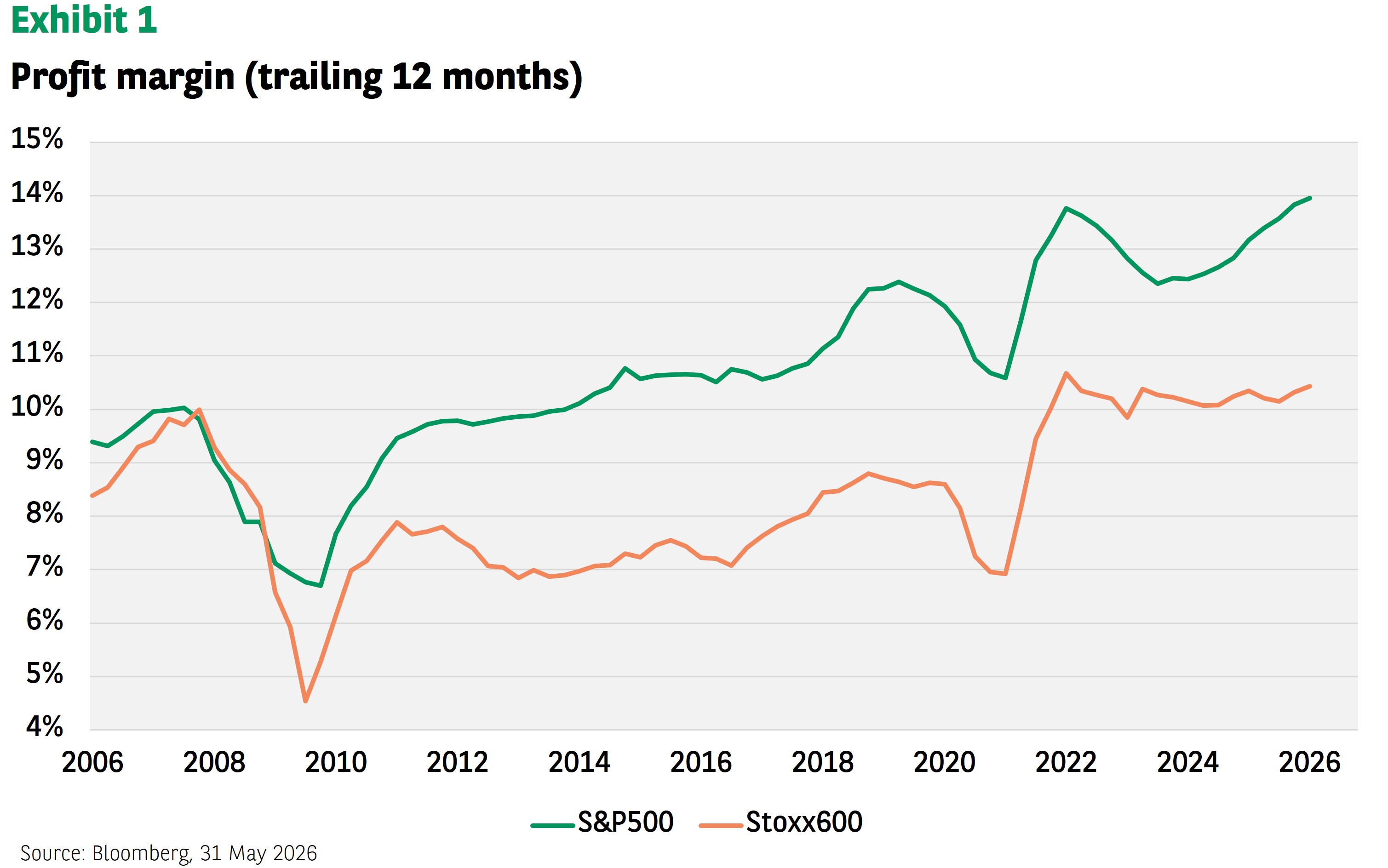

Chart of the week

Corporate America’s profitability continued to improve in Q1, further widening the gap with European companies. While the sustainability of such high profit margins may come under scrutiny in the future, in particular at a sector level, the current trend puts relative stock market valuations into a different perspective. In fact, the S&P 500 index’s price-to-earnings ratio ends up being much closer to that of the Stoxx Europe 600 index, after accounting for the difference in profit margins. Ultimately, the valuation gap between Europe and the US reflects a 1990s-style productivity boom at a time of rapid and disruptive technological change.

Words of wisdom

Chips Act 2.0: The European Commission has introduced new measures to boost its semiconductor industry, building on the original 2023 Chips Act. Part of a broader European Technological Sovereignty Package, the EC aims to also boost its capacity in artificial intelligence development, cloud and open source computing, to reduce dependencies on other markets and increase its competitiveness and resilience. It also intends to triple data centre capacity in Europe over the next five to seven years and support a more co-ordinated approach to AI across member states.

What’s coming up?

Monetary policy is in focus this week. On Tuesday, the BoJ and the Reserve Bank of Australia hold their respective monetary policy meetings. The Fed follows with its own rate setting meeting on Wednesday, while the Bank of England meets on Thursday. In terms of economic data updates, both the eurozone and UK publish their latest inflation figures on Wednesday, followed by Japan inflation on Friday.

Read more insights at the Investment Institute

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.