Take Two: Stocks enjoy strong first half; Eurozone inflation falls

What do you need to know?

Global stocks enjoyed a strong rally in the first half of 2026 as optimism over technology shares and artificial intelligence-related developments offset concerns over the Middle East conflict. Last week, the US Dow Jones Industrial Average index closed at a new record level, while the S&P 500 and the tech-heavy Nasdaq recorded their best quarters since 2020. Overall, in the first half of this year, the Dow and S&P 500 each notched up gains of 10% while the Nasdaq and the MSCI World NR indices respectively rose by 13% and 10%.*

* Source: FactSet, US dollar terms. Data as of 30 June 2026.

Around the world

Eurozone annual inflation dropped by more than expected in June to 2.8% – down from 3.2% in May and forecasts of 3%, a flash estimate showed. Last month the European Central Bank hiked its benchmark interest rate by 25 basis points to 2.25% in an effort to curb inflationary pressures. Core inflation – excluding volatile energy, food, alcohol and tobacco prices – eased to 2.4%, from 2.6%. Meanwhile, a 50% tariff on almost half of the European Union’s steel imports came into effect last week, in a bid to protect its industry from overcapacity.

Figure in focus: 162.83

Japan’s yen hit a 40-year low last week, reaching 162.83 against the US dollar. The yen has been impacted by ongoing concerns about the government’s fiscal plans and the slow pace at which the Bank of Japan has been adjusting rates. The yen has fallen around 4% against the dollar this year, reviving speculation that authorities may intervene in the market again after spending a record ¥11.7 trillion (around $74 billion) in April and May on shoring up the currency. Meanwhile, Japan’s Tankan sentiment index of large manufacturers rose to its highest level since 2018 in June, as inflation expectations rose.

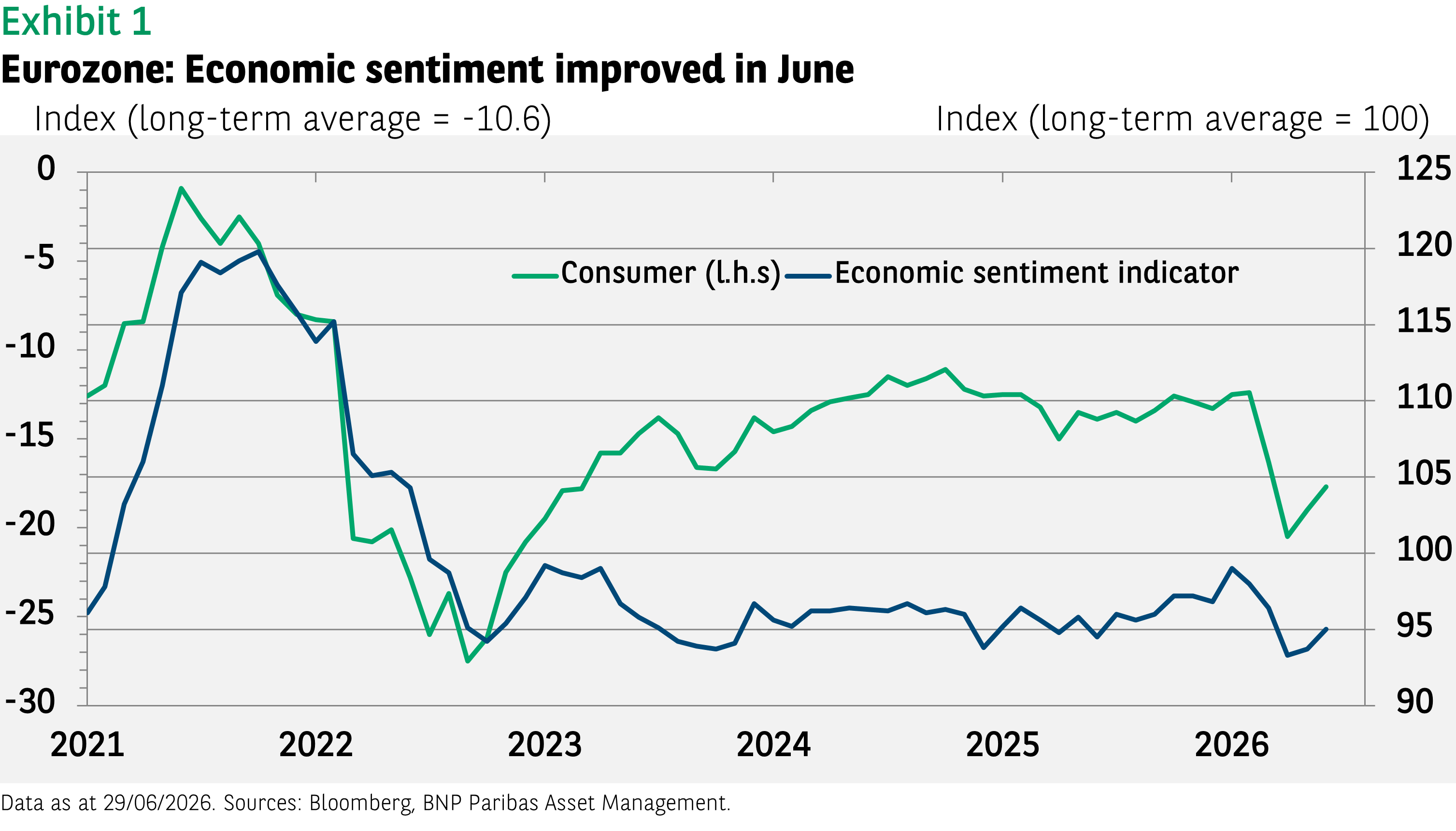

Chart of the week

Europe’s business and consumer surveys improved noticeably in June, reflecting higher confidence in all sectors, apart from construction. The economic sentiment indicator rebounded to 95 in June from 93.5 in May. Other measures delivered a similar message of economic recovery, following the impact of the Iran conflict. Selling price expectations peaked in April, and signs of inflationary pressures eased in June. However, the economic sentiment indicator is still below its long-term average of 100, and the employment expectations indicator fell by more than two points to 92.2 (versus 98 in January). The shock has not gone away entirely, and businesses appear cautious.

Words of wisdom: Helium-3

Helium-3 is a rare and very expensive isotope – atoms from the same chemical element – which can be applied to quantum computing and nuclear fusion. Currently, almost all global supply depends on the radioactive decay of tritium, a form of hydrogen used in nuclear weapons. As demand is expected to rise, and earth’s natural reserves such as gas fields only contain low concentrations, some companies are seeking alternative ways to supply the isotope. As such, lunar mining technologies are being developed with the possibility of extracting helium-3 from moon dust, where it accumulates in a higher concentration.

What’s coming up?

On Monday, the US issues its final composite Purchasing Managers’ Index for June – the flash estimate tally was 52.2, up from 51.5 in May. Both the US and Canada share their latest import and export reports on Tuesday. Wednesday sees the Federal Reserve publish the minutes of its latest monetary policy meeting where it held interest rates steady at 3.5%-3.75%. On Thursday, China updates markets with its June inflation rate – May’s figure came in at 1.2%, matching April’s total. On Friday, Canada publishes its latest employment figures.

Read more insights at the Investment Institute.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.