Mexico – Time, patience and cold blood

KEY POINTS

A complicated relationship

Mexico accounted for 16% of US exports in 2023 – second only to Canada and on a par with total exports to the Eurozone – and one quarter of the entire US trade deficit, while the US accounts for 83% of Mexico’s exports. As such, trade developments will again be the number one post-election issue for these two countries. This suggests a bigger impact if Donald Trump beats Kamala Harris. As part of the United States-Mexico-Canada Agreement (USMCA) trade deal, we would expect Mexico to be exempt from any blanket 10% tariff as threatened by Trump, in theory boosting US demand for Mexican exports as alternatives become more expensive.

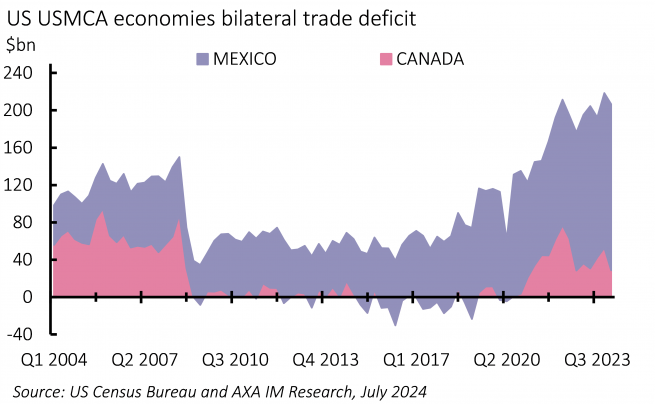

Yet there are several frictions from a Trump perspective. The US deficit with Mexico has doubled over the last five years and is now close to China’s as a proportion of the total US shortfall (Exhibit 7). Moreover, China has materially increased investment in Mexico, pouring investment into manufacturing facilities to produce goods for export into the US that bypass direct tariffs. Trump has stated he will impose a 100% tariff on Chinese produced electric vehicles (EVs) from Mexico, seemingly despite the trade deal, while Trump’s broader antithesis to US EV adoption presents a further risk. Both are likely to cause Mexico difficulties when it comes to the USMCA trade deal renegotiation in 2026, which could be difficult under either candidate. In 2017, the USMCA identified “non-market economies” (China) and restricted trade agreements allowed with them. More recently, the Inflation Reduction Act identified (although did not precisely define) “foreign entities of concern” (China). The USMCA renegotiation could well include provisions along these lines, leaving Mexico in a tricky position with regards to Chinese investment, particularly if geopolitical tensions between the US and China deteriorate. Additionally, any restrictive changes to the USMCA would also impact trade with Canada – Mexico’s second largest export market.

Previously, Trump has used trade negotiations as leverage over other policy areas and we envisage two flash points. Fentanyl is the largest cause of death of US in 18-to-45-year-olds and most is believed to arrive from Mexico. US Republican senators have suggested bombing Mexican drug laboratories and/or using Special Forces to operate in Mexico. In 2020, Mexican President Andrés Manuel López Obrador restricted US Drug Enforcement Agency (DEA) operations in Mexico, but recently tightened controls and legislation, joined the United Nations (UN)’s anti-trafficking campaign and increased co-operation with the DEA again. We expect further progress to be part of a trade deal. Moreover, Mexico has just passed judicial reform to elect judges. This was opposed by the Mexican judiciary and has raised concerns in the US, which may restrict future US investment in Mexico.

On migration, both Harris and Trump would likely slow immigration, but Trump would likely do more so and threatens deportations, which would be more disruptive. PEW Research shows in 2022 of 11mn undocumented migrants, 4mn were Mexican and 4mn Latin American (LatAm). Mexico will be wary of a revival of Trump’s first-term Migrant Protection Protocols – the “Remain in Mexico” policy. A reduction in migrants may also reduce remittances to Mexico, worth 4% of GDP – with a larger impact across the rest of LatAm – something that would also be impacted by threatened taxes. However, migration is an area where Mexico can help the US: alleviating US southern border pressure, by better controlling its own. This is leverage that might help in negotiations.

Finally, Mexico will be particularly vulnerable to US economic spillovers. Our expectation for higher US inflation, a stronger dollar and less monetary policy loosening under Trump would increase pressure on the Mexican central bank, Banxico, which has only lowered rates by 50bps from its 11.25% post-pandemic peak. This would further weigh on the Mexican growth outlook, as would the slowdown in US activity expected under a Trump presidency and any reduction in Chinese investment in the event of more restrictive conditions in a renegotiated USMCA.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.