Euro Long-Term Credit

KEY POINTS

In coming years, institutional investors with liability constraints, such as pension funds and insurance companies, could face significant challenges from the changing economic and regulatory environment. We believe that a portfolio of long-term euro-denominated investment grade credit could help them meet their liabilities while providing a positive ESG and climate profile.

The historically rapid rise in interest rates seen over 2023 has resulted in improved funding and hedging levels, as investors have oriented portfolios towards the higher rate environment. However, as a result, investors have had to manage higher cashflow needs in the medium-term while looking to lock-in the positive funding levels that have been achieved, before the economic reality changes again.

We believe there is now an opportunity to de-risk portfolios using long-duration credit strategies that match their long-term liabilities.

Investing for future needs with long-term credit

Macroeconomic background: higher for longer rates

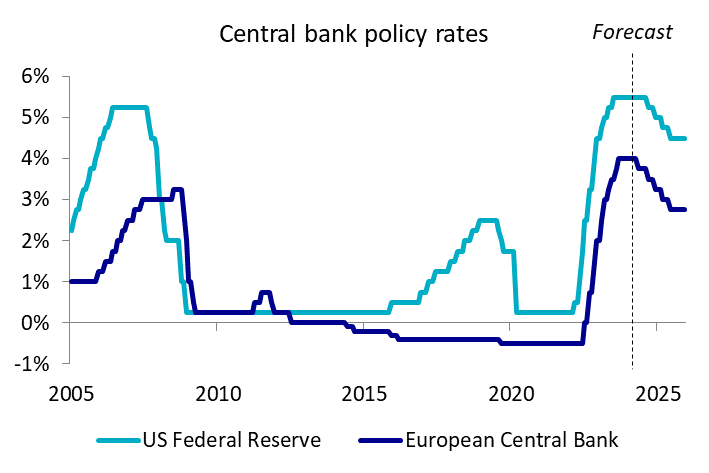

After decades of low interest rates, even reaching negative territory for some fixed income asset classes with long maturities, rising inflation since the end of 2022 has forced central banks to hike rates sharply. While we believe that the third quarter of 2023 saw rates peak, inflationary pressures are likely to remain in the near future, meaning rates will remain high and yields continue to be attractive.

Central Bank policy rates will remain higher than the previous decade

Source: AXA IM Research, May 2024

Eurozone core inflation predicted to remain above 2% until end-2025

Source: Eurostat, AXA IM Research, as of end-March 2024.

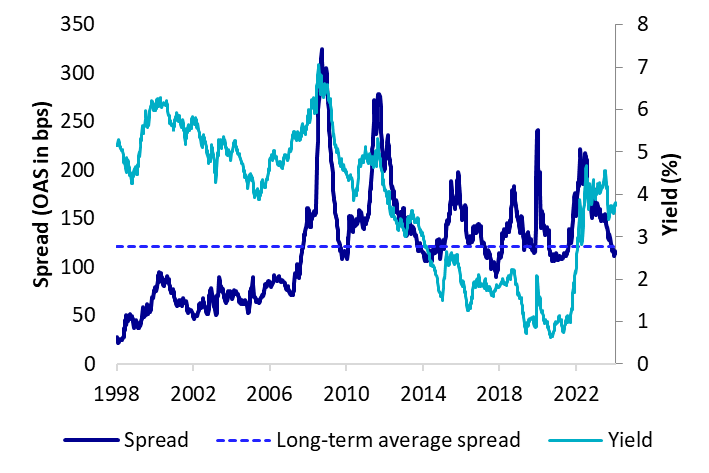

Attractive euro credit spreads pick-up versus government bonds

Long-term investment grade credit in euros currently provides 114 bps of spread pick-up over government bonds (based on the ICE BofA 10+ Year Euro Corporate Index, as of 28 March 2024). While the asset class has been on a bullish trend over the past year and a half, we see spreads remaining attractive for three reasons:

- Sound fundamentals - Corporate fundamentals are currently quite sound, with net leverage at around 2.5 times, on average, close to the 20-year long-term average. While revenues and margins are decelerating, credit metrics are resilient, with more rating upgrades than downgrades. Guidance from company management and analysts remains conservative given the growth outlook for the next two years. For financials, after two exceptional years for earnings, the situation is also very good on average, with limited exposure to commercial real estate loans for most of the European banks.

- Attractive valuations - In absolute terms, valuations remain attractive compared to the historical average. Spreads have grown tighter for almost two years, but we are still well above the floor reached in 2018.

- Comparison versus dollar credit – In relative terms, investment grade credit in euros has been more attractive than US dollar credit since 2022, and still offers around 20bps of spread pick-up (as of 28 March 2024).

Yields have broken through the 3% ceiling

Source: AXA IM, Bloomberg as of 3 May 2024. Long-term Euro credit IG universe represented by the ICE BofA 10+ Year Euro Corporate Index (ER09).

Credit carry is decent, albeit close to the long-term average

Source: AXA IM, Bloomberg as of 3 May 2024. Long-term Euro credit IG universe represented by the ICE BofA 10+ Year Euro Corporate Index (ER09). Carry: return coming from the yield, i.e. total return of a bond assuming that the yield does not change.

Credit can be an alternative to derivatives for liabilities hedging

Many investors use high-quality bonds as a natural hedge for their liabilities, which are subject to similar interest rate sensitivity. Managing liabilities using only derivatives was shown to have some limits during the UK gilt crisis in September 2022 – long-term contracts can still trigger meaningful short-term collateral needs, and market conditions can make it complicated to withdraw cash in stressed times. Reducing the use of derivatives and using cash bonds instead can provide a buffer of carry and absorb some market volatility.

A large and liquid universe

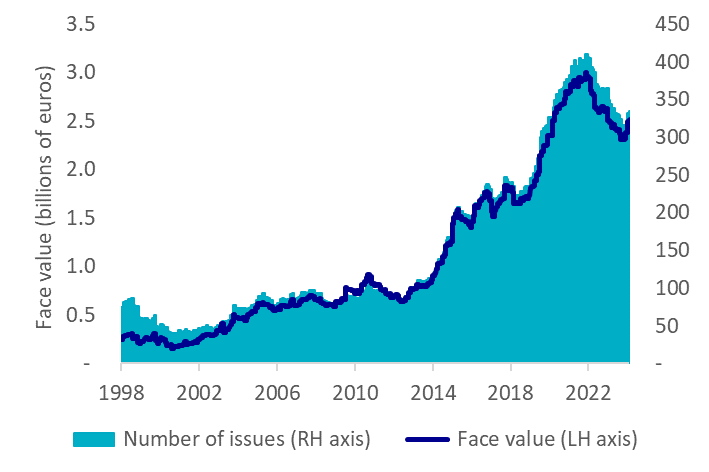

Fixed income credit markets have been growing over the years, offering high levels of diversification by region and sector, and across the curve. We believe that credit markets have sufficient market depth to build an efficient portfolio solution for tackling liability requirements on the long end. Liquidity can be challenging during periods of market stress, but high-quality bonds tend to be more liquid in these conditions. Access to primary markets is also a great tool to manage liquidity.

Long-term euro credit investment grade market has grown rapidly since inception

Source: AXA IM, Bloomberg as of 30 April 2024. Long-term Euro credit IG universe represented by the ICE BofA 10+ Year Euro Corporate Index (ER09).

Case study: Euro Long Term Credit strategy – locking-in attractive carry

Many of our institutional clients are looking for long-term interest rate exposure to meet their liabilities and lock-in current attractive yields in a cautious fashion. To address this, we have developed a Euro Long Term Credit strategy that aims to deliver total return performance of high-quality investment grade credit with an average duration around 15 years.

The strategy applies a conservative approach and invests only in A- rated issues or better, with a strong focus on euro-denominated bonds. It aims to comply with Article 8 of the SFDR regulation. We think that limited exposure to US-dollar and sterling credit helps provide resilient long duration exposure, and so allow up to 30% allocation to foreign currency credit within the portfolio (namely USD and GBP denominated bonds), hedged back to euro.

We also believe that, at the very long end, quasi-sovereign entities provide attractive spread pick-up with the additional benefit of long rate sensitivity.

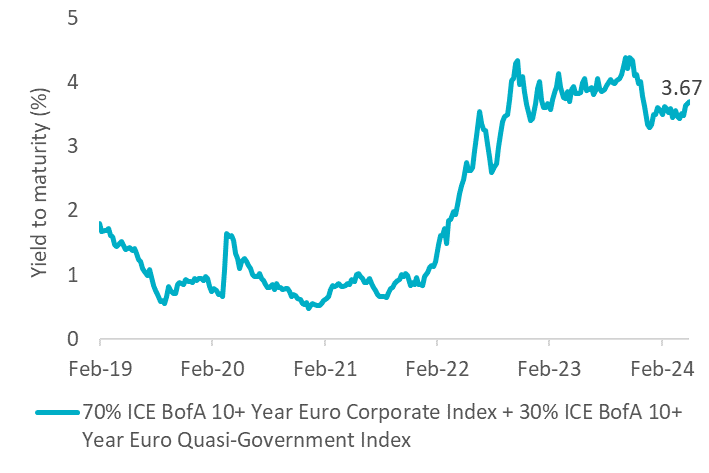

Illustrative benchmark: 70% 10y+ Euro IG Corporate + 30% 10y+ Euro Quasi-Government index

Source: AXA IM, ICE, Bloomberg as of 30 April 2024. NB: This illustrative benchmark includes BBB-rated bonds and has a lower duration than the Euro Long Term Credit strategy target (15 years). In addition, non-euro bonds are not included.

Strong fundamental credit analysis gives us a high level of confidence in our holdings, and so we prefer a ‘buy and maintain’ approach, which helps limit portfolio turnover to 10-20% a year. This annual turnover budget is used mainly to sell bonds with residual maturities between 10 and eight years in order to keep portfolio duration in-line with its 15 years objective.

As a long-term responsible investor, ESG matters are key to us and are systematically included at every stage of our investment process.

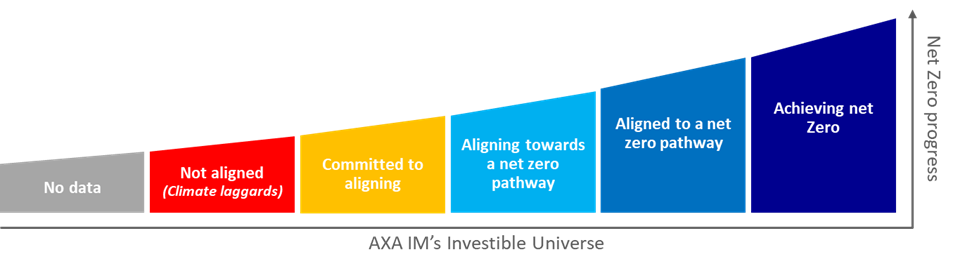

One of the aims of this strategy is to contribute to a low-carbon economy by reducing the portfolio’s carbon footprint. We use AXA IM’s proprietary Carbon Transition Framework to help us invest in issuers that are committed to achieving net zero carbon emissions, and avoid ‘climate laggards’ that have no clear carbon transition pathway or credible targets. This framework enables us to track issuers’ progress on their Net-Zero alignment journey, using both quantitative and qualitative research, leveraging the Net Zero Investment Framework from the Paris Aligned Investment initiative.

Source: AXA IM

In addition, we believe that engaging with the issuers is a vital part of supporting the transition to a low carbon economy. Through our engagement activities, we aim to help issuers set and meet their decarbonisation targets, and appropriately escalate our engagement where we believe that issuers are not moving fast enough.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.