As the dust settles European financial sector still offers opportunities

- 25 April 2023 (5 min read)

Key points:

- A useful reminder of the power of sentiment in markets

- The fundamentals of euro banking sector remain positive

- What the March panic might mean for banking and financial sectors

Across the financial sectors, March proved to be a surprisingly volatile month prompted by the Silicon Valley Bank (SVB) collapse that was swiftly followed by the rescue of Credit Suisse by UBS. With sentiment likely to remain fragile for some time, we take a look at the fundamentals of the European financial sector and why we are still positive on it.

Following the wave of fear prompted by the Silicon Valley Bank (SVB) collapse and other small regional banks in the US, markets plunged into further darkness a few days later, with Credit Suisse's share falling as much as 30% intraday. The European Financials sector was severely impacted as other banks also plunged in a panic reaction. While the impact on debt repayment in this higher interest rate environment was always going to cause challenges for some issuers, what particularly shocked the markets over the Credit Suisse event was the treatment of Additional Tier 1 (AT1) which the regulator decided would absorb losses ahead of equities.

While this treatment emphasises the risk of this particular part of the capital structure, the Credit Suisse event seems to be a single episode. Partly as it was not a surprise that the bank may need to be merged with another bank and partly because the European Union was quick to assure investors that AT1 assets at other banks remain above equities. As the chart shows, the high spread dispersion suggests idiosyncratic risk rather than systemic risk.

Source: Bloomberg, IHS Markit, AXA IM Research calculations as at 21/04/23

Strong fundamentals

We believe the fundamentals for the financial sector, overall, are strong and we expect 2023 to deliver positive growth for the sector. The Q4 2022 earnings on European banks were strong, beating expectations thanks to a high net interest margin and benign cost of risk. We expect profitability to rise further for most banks in 2023, as we have seen for some of the US Banks in the latest earning releases. We also expect to see only a moderate rise in impairments and asset quality deterioration as the eurozone avoids recession.

Despite fundamentals being strong for the financial sector, the recent events on SVB and Credit Suisse have shown that sentiment can prevail. Indeed, following Credit Suisse other European banks, such as Deutsche Bank, Commerzbank and Société Générale were hit by a new episode of volatility affecting their equity and bond prices. In a market environment where sentiment drives financial stability, the impact sentiment has on fundamentals is easy to see. SVB failure is a stark reminder of how confidence is absolutely necessary to banks’ stability, and of how complete loss of it may push them to the brink very quickly via a deposit-run.

It has also been a good reminder on the value of being protected within a capital structure such as senior bonds are, and that for riskier assets like AT1, being properly remunerated for that risk is paramount.

Regulatory environment differ from the US market

Banks in European countries operate under very different regulatory conditions to those in the US. While in the US, largest banks are heavily regulated and stress-tested, smaller banks are not put under the same level of scrutiny. Just taking Basel III standards, 300 European banks are signed up to the Basel III standards that require all banks that are internationally active, regardless of size, to maintain certain liquidity and capital requirements. In the US only 3 banks are under Basel III.

Of course, liquidity crises happen even with strong regulation, and European banks are as exposed to rising interest rates and the impact that could have on debt portfolios, however operating and funding models of European banks look very different to US ones.

The European Central Bank also has tools that should support the market as whole making the fear of contagion for European banks following an individual bank’s demise seem less likely.

What next?

Already, the credit default swap spreads for European non-financial and financials are moving back to pre-SVB levels suggesting that the worry over banks is ebbing in Europe.

Europe: iTraxx Senior Fins (green) vs iTraxx Non Fins (orange)

Source: Bloomberg, IHS Markit, AXA IM Research calculations as at 21/04/23

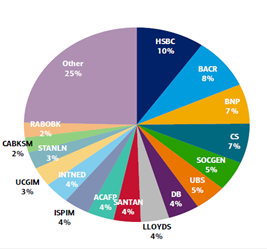

A broader impact from this turmoil may be seen in the pricing of debt, at least in the near term. Credit Suisse was amongst the biggest AT1 issuers in the market with 7% market share, predominantly in USD. After the Credit Suisse AT1 write-off, we have seen sharp repricing in the market segment but not a full recovery yet. Investors are likely to demand higher premium going forward.

Overall, we remain positive on the sector although cautious and continue to monitor the situation closely, especially for any signs of potential contagion. As we saw in March, failure can be sentiment-driven, with soured sentiment impacting highest beta names and those already under close market scrutiny the most. While we see strong fundamentals and a positive outlook for the sector, we are aware that market developments and sentiment will be key.

Fixed Income

We cover a broad spectrum of fixed income strategies to help investors build diverse portfolios that can be more resilient to economic and market shifts.

Find out moreDisclaimer

This document / video is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.