Time to look at fixed income again?

- 03 March 2022 (7 min read)

What’s been happening? The perfect storm.

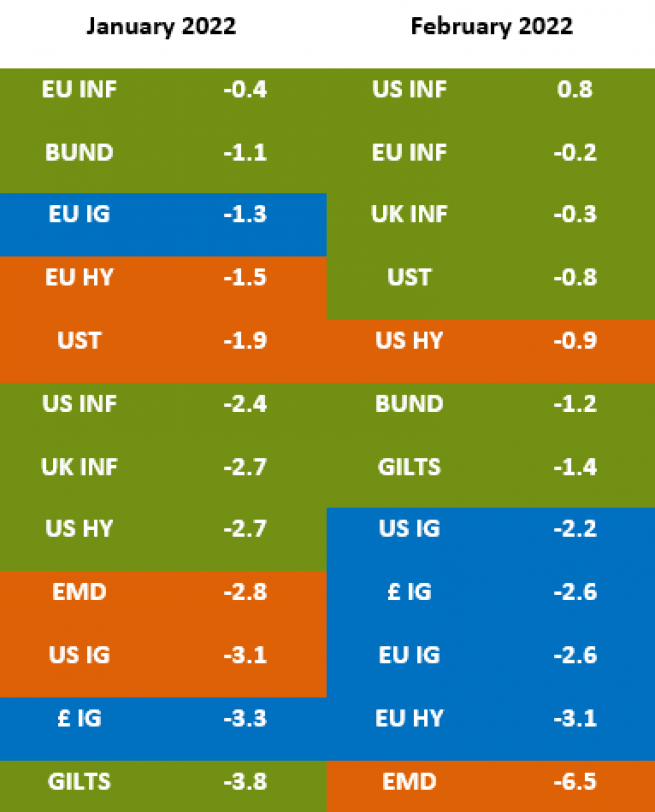

It is fair to say that 2022 has brought with it a fair amount of challenges – both on a geopolitical and humanitarian level but also in terms of market volatility. January and February were, by many measures, the toughest months for many asset classes for a long time – with significant macro headwinds including continued higher inflation, supply chain issues, surging energy prices as well as the escalation of tensions between Russia and Ukraine, which combined to create a negative environment for both bonds and equities.

In this sort of environment, with correlated negative returns across asset classes, generating positive returns in the context of a long-only fixed income strategy is clearly challenged. That said, it is worth bearing in mind that the environment that we have seen in 2022 is pretty rare – in fact if we look at the 12 market indices broadly representing the strategy’s investible universe, we very nearly recorded the first instance of consecutive negative total return months across all indices during the 10 years that we have been running a global strategic bond strategy. Indeed, January was just the fifth month that a full set of negative returns has ever occurred over 117 months of data.

Higher yields, higher carry

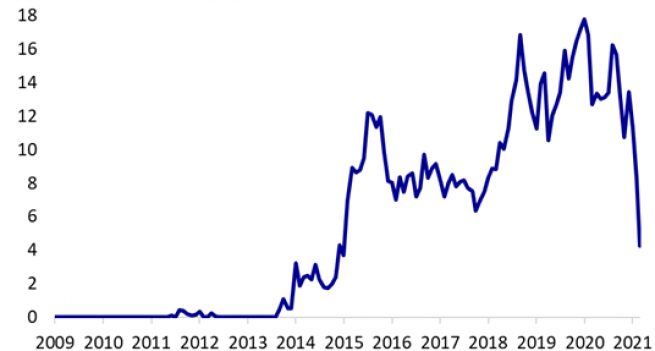

The positive for bond investors is that markets have been pricing in an awful lot of good news as economies rebound from COVID-19-related lockdowns. This means that fixed income investors are investing into a much cheaper asset class than the one that we have become accustomed to in recent years – dogged by low/negative yields and tight spreads. See below, for example, a chart indicating the amount of negative yielding debt globally ($ trillion), which barely existed prior to 2014 and reached a peak of $18 trillion in 2020. In just over a year that amount has come down to $4 trillion in light of the current market sell-off, which can only be encouraging for an asset class that investors are drawn to, amongst other reasons, for the positive income stream it offers.

Moving forward, this starts to make us quite excited about the potential for generating attractive returns through a combination of higher carry and price movement, albeit in the short term our focus is on navigating the current bout of heightened market volatility.

Russia/Ukraine crisis

Dealing first with the Russian invasion of Ukraine, our strategy has very limited direct exposure to Russia/Ukraine holdings. As you might expect, liquidity around these names is currently very poor so we continue to monitor the situation closely before deciding on what to do with these positions. More broadly, as communicated by our economists and strategies, the situation remains very much in flux but from a central bank perspective, although clearly there will be an impact on global growth, felt particularly acutely in Europe, this should be offset by the inflationary effects of even higher energy prices – given the dependence on Russia for oil and natural gas supplies. In this environment, we still expect monetary tightening to go ahead, given concerns that higher inflation could become entrenched, but it should be gentler than previously anticipated – and certainly we think not as aggressive as the market currently prices (more on this below). If anything, a general risk-off sentiment should create a positive technical dynamic for safe havens such as government bonds which we have started to see come through in the past couple of days, although the inflation story and rate hikes still, for now, loom large.

Government bonds / duration: the ‘bear flattener’

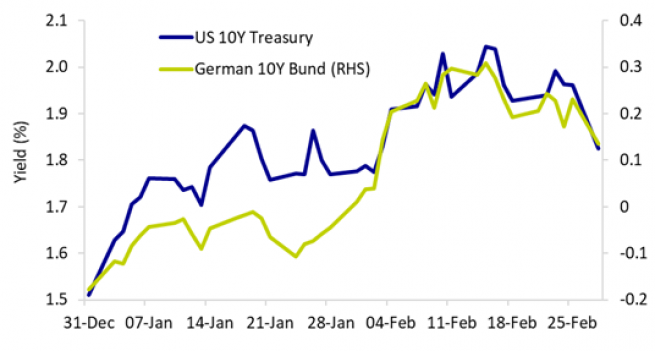

Turning to markets, government bond yields have headed higher in light of increasingly hawkish messages from central banks with regards to interest rate rises to curb inflation, with the short end particularly affected – leading to a strong flattening of the curve. As the chart below shows, for the first time since 2019, US 10-year treasuries went through the much heralded 2% yield level, although have since rallied back, and German 10-year bund yields also turned positive.

Even if there has been a consensus view that elevated and persistent inflation will push increasingly hawkish central banks to shift policy towards a higher interest rate environment where, on the face of it, core government bonds should suffer in the short term, being structurally short duration, or even negative duration, does not strike us as a strategy that will bear fruit in this environment given a few important factors that may continue to put something of a cap on yields irrespective of any impact from the situation in Ukraine:

- Higher yields are leading to a pick-up in asset class volatility and lower equity stocks, especially in the Technology sector. At some stage, this should lead to lower yields as the safe-haven nature of government bonds comes to the fore

- From a valuation perspective, bond yields have been moving steadily higher for more than a year and last week priced in around six rate hikes from the Fed in 2022. Although this may be accurate and the Fed have not ruled out hiking at every meeting this year, we would argue that bond yields have been moving towards ‘fair value’ meaning that, at worst, the return over the life of the asset should equal the carry and, at best, that the tightening conditions of higher yields, along with more volatile equity markets, might lead to slowing growth and less need for rate rises, which the market might be overestimating. In this environment, bonds should rally and generate a decent total return

- The Fed’s expected ‘lift off’ is leading to a bursting of many asset class bubbles, which have been building for many quarters as QE has continued to be pumped into markets. Eventually, this should be good for fixed income, albeit there may be some short-term pain along the way

In our strategy, we materially reduced duration in early February, mainly by moving negative duration on the Bund curve but retaining our strong bias towards USD duration. In this sense, we have been playing a USD vs EUR cross-market trade, meaning that we think a lot of rate rises were already priced into the US, but hawkish signals from the ECB earlier in the year also led markets to begin pricing in the potential for ECB rate rises in 2022, which was somewhat unexpected. As such, any negative contribution from our USD duration would be partially offset by a positive contribution from EUR duration – assuming rates continued to move higher in both the US and Europe. Towards the end of February, we neutralised this position in light of the escalating situation in Ukraine, given that a war in Europe should lead to a less hawkish ECB. On 1 March, we saw a huge risk-off move and a strong rally in the bond market, leading us to add yet more duration to potentially benefit from this momentum.

There has also been a lot happening on the curve, which has continued to flatten as short-dated bonds have continued to sell off on the expectation that we will see interest rate rises in the near term. Longer-dated bonds, meanwhile, have not moved nearly as much as they continue to price in a relatively shallow hiking cycle in line with the thesis that inflation will ultimately not be permanent.

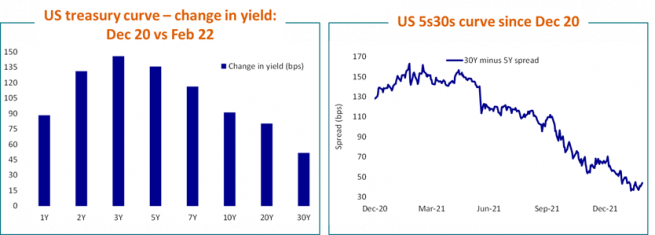

These moves are evident from the below charts – on the left-hand side you can see the change in yield at different parts of the US treasury curve between 31/12/2020 to 28/02/2022 (expressed as a spread), where the 3-year and 5-year maturities have risen much more than the 30-year. This has led to the strong flattening of the curve evident in the US 5s30s (30-year minus 5-year spread) chart (right-hand side) over the same period.

In such a ‘bear flattening’ environment (yields rising but curve flattening), we favoured the long-end versus the short-end, which has benefitted from a flattening curve even with yields rising across the board. Towards the end of February, however, we took off this 5s30s ‘flattener’ as we think that the market response to Russia’s invasion of Ukraine might be to price out some of those aggressive expectations for short-term rates, which could lead to a steeper curve. Moving forward, we think that the curve is going to be one of the key indicators for 2022 (along with CPI data and US 10-year treasury yields). A few scenarios are possible:

- The curve continues to flatten which, along with tightening financial conditions, makes it difficult for banks to lend and make money: a great predictor of recessions

- Alternatively, the Fed decide they don’t want or like a flat / inverted yield curve (because of its predictive powers) and, whilst raising rates, they decide to sell long-dated bonds back to the market (QT: ‘quantitative tightening’) to steepen up the yield curve. In this sense, they might hope to extend the economic expansion for a while longer

- A third scenario clearly relates to the impact of Russia/Ukraine on market expectations for monetary policy, which could lead to an unwind of short-term expectations for rate hikes and hence a steeper curve

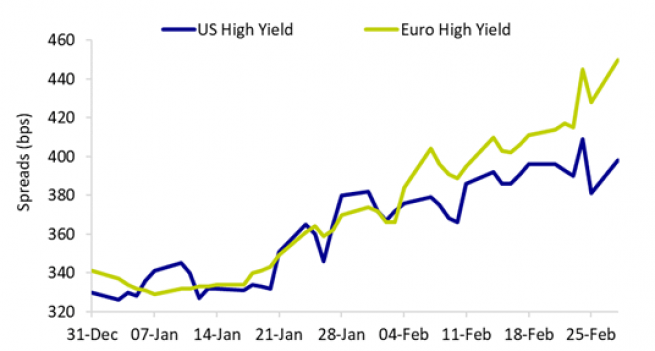

Credit / HY: spreads wider but fundamentals unchanged

In the second half of January, high yield (HY) spreads also started to widen, driven by a weakening equity market that began in early January with a sell-off in Technology stocks adversely affected by the possibility of higher rates and slowing growth, as well as the continued global chip shortage, before spreading to other sectors in the second half of the month and into February as tensions escalated on the Ukraine/Russia border.

European high yield spreads have widened further than US equivalents in February, given the greater impact of the war in Ukraine on Europe. Investment grade (IG) credit markets have also been hit by wider spreads, whilst also having to contend with higher government bond yields, leading to an underperformance in 2022 compared to high yield markets.

We maintain a strong preference for lower-rated BBB opportunities, favouring GBP / EUR markets over USD and with a particular focus on European financials. In high yield, however, from an asset allocation perspective we felt it prudent to reduce exposure to US high yield in order to be a bit more risk-off during the current volatility. That said, there have still been opportunities to add value in US high yield over 2022 so far through shorter duration positioning and careful security selection.

We think there is now an opportunity to add some duration and yield to a US high yield allocation on recent market weakness. We still favour having a defensive tilt, but less so than going into November 2021 and prior to this recent sell-off. There are also certain names affected by Omicron-related weakness (e.g. Leisure) which now look attractive.

Active CDS (Credit Default Swaps) positioning could be another useful tool – where there have been some quite sharp moves in relation firstly to the news and potential threat relating to Omicron in November and more latterly in relation to a general weakness in risk assets and the escalating conflict in Ukraine.

Emerging markets: down but not out

Within emerging markets, there has been no reprieve after a difficult 2021 stemming from volatility in the Chinese property market and the vulnerability of emerging market currencies to higher US treasury yields. In fact, 2022 has seen a continuation of these themes plus the addition of the crisis in Ukraine, which has increased negative sentiment towards the asset class. That said, although the months ahead look challenged, there will come a point in 2022 when we believe that emerging markets will look very attractively valued. For now, however, we are maintaining a relatively cautious approach. From a bottom-up perspective, we have continued to rotate our global strategic bonds strategy away from high carbon producing commodity producers into renewables and more ESG friendly credits, with most activity coming via primary issuance.

Outlook: where do we go from here?

Moving forward, we believe that there are reasons to be optimistic about fixed income returns and that the current volatility could create opportunities. Market pricing for monetary policy appears to be relatively aggressive and, if central banks disappoint the market in light of the threat to economic growth from the Russian invasion of Ukraine, falling inflation, a normalisation of demand and an easing of supply chain issues, then duration could benefit from some total return potential, on top of offering higher carry than it has done for 18 months. Similarly, appetite for risk assets still appears to be strong and we do not see default rates moving much off historic lows. Recent market weakness has slightly improved the total return outlook for the US high yield market.

It is worth emphasising that we expect 2022 to remain volatile due to the Russia/Ukraine conflict, as well as the expected shift in monetary conditions and the easing of asset purchasing programmes by central banks, so we will continue to use our flexibility and tactical portfolio hedges (e.g. futures to dynamically manage duration, CDS to adjust credit risk) to navigate through this environment. In summary, however, we would suggest that a lot has already been priced into bond markets and their ability to surprise to the upside should not be underestimated – given that consecutive negative years in bonds are incredibly rare.

Our fixed income approach

We cover a broad spectrum of fixed income strategies to help investors build diverse portfolios that can be more resilient to economic and market shifts.

Find out moreDisclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.