US reaction: Labour market achieving balance

- 05 July 2024 (7 min read)

Headline payrolls once again exceeded expectations, but this time with a degree more reality than last month’s shock. June saw the establishment survey rise by 206k. This was firmer than the 190k consensus and firmer still than our own expectation of a weaker 150k. However, this month’s release was accompanied by sharp downward revision to the previous months’ estimates of -54k for May and -57k for April. This brought headline payrolls in May back to 218k – still solid, but not as robust as first reported and closer to our initial expectation. A similar order of revision to this month’s initial estimate would leave payrolls close to our forecast. For now, the headline trend pace has already softened to 177k – its slowest in 3½ years.

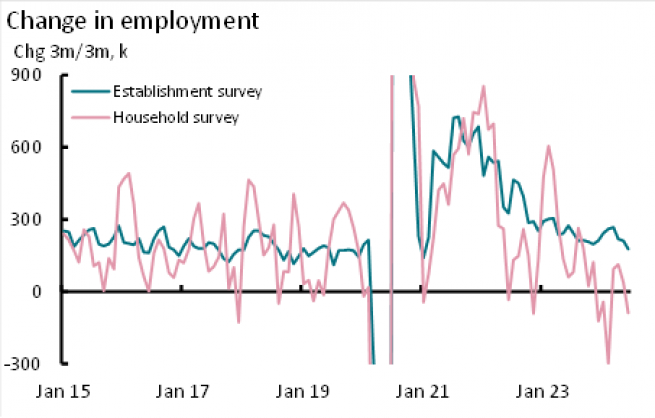

The household survey showed employment rise 116k in June after a 408k drop in May. The 3-monthly pace here is now -89k. Exhibit 2 below illustrates that employment is on a weakening trend for both measures. The household survey also showed that unemployment rose to 4.1% - its highest rate since end-2021. This rise took place despite rising employment as labour supply recovered from the steep drop posted last month, rising by 0.17% on the month, lifting the participation rate back to 62.6%, rebounding from -0.15% in May which had stopped a larger increase in unemployment then. Unemployment was just 3.6% one year ago, 0.5ppt lower and is now close to triggering the ‘Sahm rule’ – an observation that a rise of 0.5ppt in the 3m average unemployment rate over the space of 12-months has historically been a signal of an economy in recession.

June also saw a softening in pay growth, average earnings rising by 0.3% on the month following a 0.4% rise in May. The annualized 3-monthly rate of earnings growth has slowed to 3.6% from 4.0% last month (3.5% from 3.6% for non-supervisory pay) and even the annual rate has slowed to 3.9%. We have long considered 3.5-4.0% an area that the Fed is likely to deem as consistent with its longer-term 2% inflation target. If pay growth remains around current levels, we believe the Fed will consider the labour market as appropriately balanced.

In all, while today’s headline delivered a modest upside surprise, in total we see it as consistent evidence of an easing labour market and softening economy. It has not yet provided a shock to markets as we consider likely over the summer, but is gently deflating. Consistent with other indicators: a trend decline in JOLTS (despite an upside surprise here in May) and a rising trend in continuing claims, we can see why the Fed is increasing focusing on the labour market, rather than single-mindedly focused on inflation, as suggested in the minutes to June’s FOMC meeting. We expect this softening labour trend to persist over the summer, consistent with our expectation of a soft landing for US economic activity. Next week’s CPI inflation report will be the next important release, but we expect this to continue to tell a story of benign disinflation. Accordingly, we expect the Fed to cut rates, not this month, but in September and again in December.

Financial markets saw no change to the probability of a September cut, pricing that around a stable 75% chance, but December saw a small rise in chance of two cuts to above 80%. After an initial knee-jerk reaction, term rates also edged lower, 2-year US Treasuries -4bps to 4.64% and 10-year -2bps to 4.31%. The dollar was marginally lower, but having already softened 0.2% today and 0.7% since Wednesday morning’s weak services ISM print, the dollar has already traced some ways.

Related articles

View all articles

European Parliament and French elections: Investor update

- by Gilles Moëc, Chris Iggo,

- 24 June 2024 (10 min read)

US reaction: CPI notches 2nd confidence builder

- by David Page

- 12 June 2024 (3 min read)

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.