Eurozone - It's not over yet

- 02 December 2020 (3 min read)

Key points

- Good news on the search for a coronavirus vaccine is unlikely to change the macro trajectory before mid-2021 – we expect a weak end to 2020 and a shallow recovery in the first half of next year.

- But by providing a horizon to normal sanitary conditions, it should help governments to opt for more generous stimulus: deficits will remain large.

- The ECB will make sure it does not really matter: implicit yield curve control is on the way. This will require flexibility. Discussions on the limits won’t be easy though and should be seen in the broader context of revamping Brussels fiscal rulebook.

2020 not ending fast enough

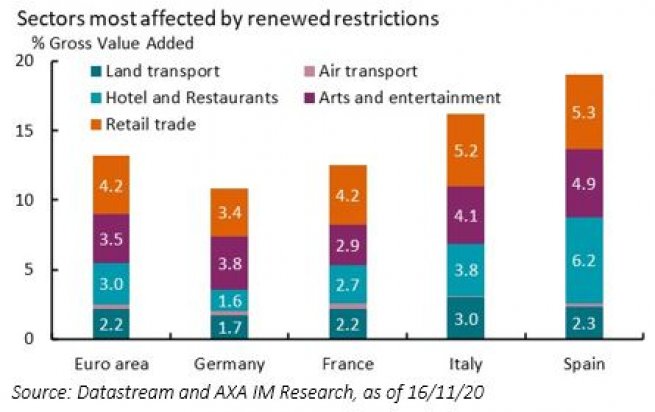

For Eurozone economies, 2020 cannot end soon enough. After a 15.1% decline in the first half of the year and a strong, but partial, rebound in the Q3, the euro area economy is set to contract again in Q4 (-4.1%qoq). The autumn lockdowns triggered by the pandemic’s second wave are less restrictive than in the spring (schools, the public sector and industry remain open this time), and so is our assumption of activity hit (-10% in November on average for the euro area versus around -25% in April). But the euro area will finish the year 8.3 percentage points (ppt) below end-2019 levels and with large dispersion across countries. Virus developments, stringency of restrictions, exposures to the most affected sectors (Exhibit 1) and fiscal supports vary across countries. For that reason, we see German growth shrinking by “only” 6%yoy in 2020, half of the contraction we expect in Spain, and much better than the 7.7% decline we project for the euro area as a whole.

A vaccine will boost growth in the second half

We expect a shallow recovery in the first half of 2021. The news of a vaccine from Pfizer and Moderna is positive, helping dispel concerns that the lockdown/re-opening pattern and its persistent damage to trend growth would be permanent. Yet its near-term growth impact should be limited in our view – production and distribution capacity constraints suggest herd immunity may not be reached before the summer. In the meantime, we think governments will keep in mind a key lesson of the summer experience: in an imperfect testing/tracing environment, restrictions must be lifted gradually.

Despite a potentially positive confidence boost from the vaccine, countries have entered their second wave on a weak footing, having managed only partial repair from the first. Eurozone consumer confidence had plateaued over the summer and edged down in October even before stringent restrictions were announced. Although the labour market impact has been largely cushioned by short-time working schemes, the number of unemployed has increased by 15% since February and there are multiple signals of a job-poor recovery: employment fell by 2%yoy in Q3 and firms hiring intentions are down in both the services and industry sectors. In this context, precautionary savings should remain elevated in the months ahead, capping household spending.

Exhibit 1: One aspect of internal divergence

The flipside is that corporates will continue to see demand as a key factor limiting production. Once again, this comes while activity levels have not fully recovered from the first wave. Even in the less affected industry sector, the capacity utilisation rate is still 6% below its pre-crisis level - it has barely improved from a record low in the services sector. Despite the help from short-time working schemes, profits have been squeezed, credit risks are piling up - banks have tightened credit standards on corporate loans already and expect further tightening in Q4 – and debt has risen sharply. This is not conducive to stronger investment, even without mentioning the risks of rising bankruptcies. So far, these have been suppressed by temporary regulatory forbearances, but demand may not pick up quickly enough to avoid them.

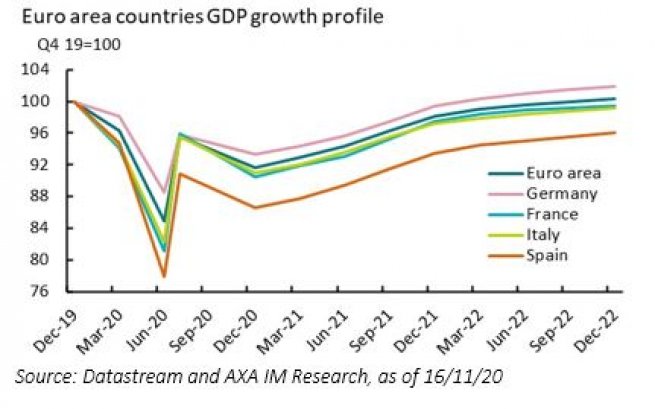

The broad deployment of a vaccine should allow for a full unwinding of containment measures, leading to some growth acceleration in the second half of 2021. A supportive external environment will add to a significant bounce-back of the domestic hospitality sector. Household consumption (precautionary savings to be unleashed) and exports (rising tourism) should fuel the recovery, but an investment rebound is likely to be capped by the debt legacy. In Q4 2021, we see euro area private consumption just 3.2% below its pre-COVID-19 level, but investment still 8.1% lower. Overall, the Eurozone should round off the year with 3.7% annual growth, followed by another solid 4.4% in 2022. Still, the economy would only be back to its pre-pandemic level at the end of our forecast horizon (Exhibit 2).

Exhibit 2: A long time to come back to square one

Enabling “last mile” policy support in the first half of 2021

If we think the vaccine boost to growth will be limited in the near term, we nonetheless believe it will have a strong and early impact on economic policies. The perspective of restoring normal conditions at some point in the second half of 2021 should make policymakers more generous with their stimulus. Indeed, if the first half of the year is the “last mile”, then fiscal authorities should be less worried about the risks of an endless drift in public debt and take the risk of providing more support in the months ahead.

This would be particularly relevant for Spain, which has adopted a slightly more hesitant fiscal approach so far. Indeed, fiscal stimulus in 2020 has been broadly similar across countries at around 4.5 to 5.5% of GDP, but the GDP loss, as discussed above, has not – meaning that Germany has done relatively more, and moved earlier, than Spain to repair its economy. For 2021, Spain is betting heavily on the Next Generation EU package funds (€27bn), but disbursement will not happen before the second part of the year and will only peak in 2024. On a side note, we remain constructive on the resolution of the rule of law standoff: the economic – and probably geopolitical – pain for Poland and Hungary would be too significant for them to actually veto the EU budget.

Germany, France and Italy did not wait for the vaccine to boost their fiscal responses. Renewed lockdown pushed France to shift its fiscal cliffs, extending short-time work and state loans guarantees schemes. In addition, the quantum of help to enterprises has increased. Germany announced a €10bn support package to pay 70 to 75% of revenue losses to businesses directly affected by the November lockdown and an extension of the bridge-funding fixed-cost grants for business until mid-2021. In France, eligibility for the solidarity fund payments has been eased and payments are being more generous than in the spring. The same is true in Italy, with a €8bn package. We believe the vaccine will make it easier for these damage control measures to be extended well into Q1 and could even spur some proper demand stimulus. One obvious consequence is that 2021 deficits – and debt – will be larger than planned in the Budgets sent to the European Commission in mid-October. We think the European Central Bank (ECB) will make sure this has no adverse impact.

The ECB – in it for the long haul

ECB support during the first phase of the pandemic has been prompt and swift, ensuring easy financing conditions and reducing fragmentation. More is coming in December to face the second wave. At the ECB Forum on central banking, President Christine Lagarde suggested that the Pandemic Emergency Purchase Programme (PEPP) and the Targeted Longer-Term Refinancing Operations (TLTROs) will remain the tools of choice. We expect a top-up of the PEPP by €500bn with an extension until end-2021, with reinvestments until end-2023, and more generous TLTROs, with a longer discount period until end-2021 at least, and potentially a lower dual rate.

But beyond the short-term monetary policy hints, Lagarde seized the opportunity of the ECB Forum to explicitly unveil a strategic shift, which to some extent pre-empts the conclusions of the review which has barely started (and where we expect symmetric inflation target and some implicit form of average inflation targeting) . By saying that “monetary policy has to minimise any ‘crowding-out’ effects” of fiscal policy, she is de facto engaging the ECB in an implicit yield curve control. This means that a relaxed approach to the ECB limits should be here to stay. Indeed, the central bank can hardly tell governments “we have your back” and then withdraw support because their holdings of sovereign bonds have reached a certain level. In the near term, this has only limited implications – flexibility is embedded in PEPP, and an extension until end-2021 seems (almost) a done deal.

Yet things might get a bit bumpy towards the end of 2021. By that time, as per our baseline the euro area will no longer be in a proper “state of emergency”. Maintaining PEPP beyond such point would be difficult to justify. True, inflation would still be below target at 1.5% as per the ECB’s latest forecasts – artificially boosted by upward base effects due to the reversal of the German Value-Added Tax rate cut. This alone would mean the monetary policy stance will have to remain accommodative. Fiscal policy will also probably need to remain supportive, as output gaps would still be significantly negative. This should call for boosting the ECB’s “ordinary” quantitative easing programme, the Asset Purchase Programme (APP). A fiscally-supportive German government (with general elections in September 2021) and the Recovery and Resilience Fund – which offers another pool from which the ECB will be able to buy – might help to buy time before the APP limits bind. Still, the market may question the credibility of APP if the ECB fails to explicitly tackle the “limits” issue. Cooperation between monetary and fiscal policy needs mutual trust, and that’s why discussions in Brussels on the fiscal rulebook will be key to monitor.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.