Top Three Green Bond Myths

KEY POINTS

Despite the breadth and depth that the green bond market now offers, there are still a few hardwired misconceptions about the asset class. In this piece we want to share with you our thoughts on these myths.

Myth 1: Green Bonds offer lower yields than conventional bonds

Green bonds function as conventional bonds and their yield is influenced by various factors such as market conditions and the credit fundamentals of the issuer. Importantly, the environmental projects financed by green bonds do not directly impact the risk or performance of the issuer.

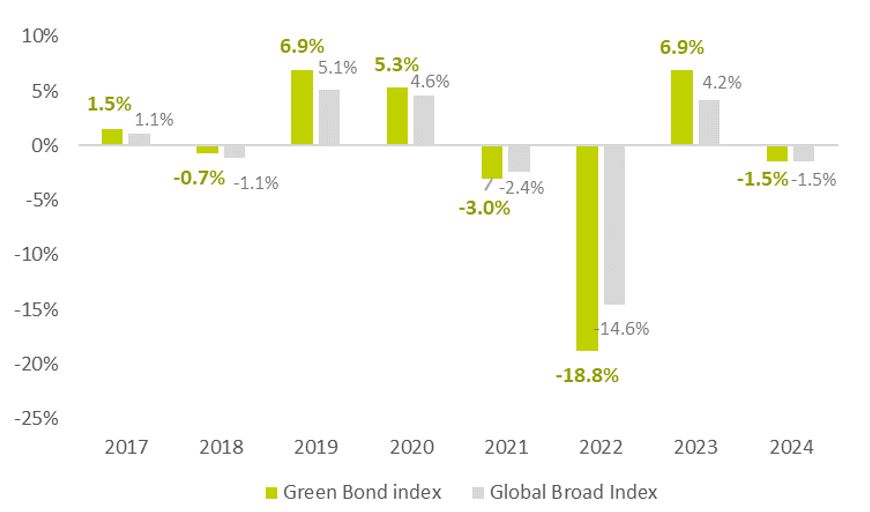

As the chart shows, green bonds currently offer attractive yields, and have outperformed the conventional universe in 5 out of the last 7 calendar years.

Calendar performance

Source: AXA IM, Bloomberg as of 29 February 2024

For investors, green bonds currently offers attractive yields while also having access to issuers who are investing in the transition to a low carbon economy. Furthermore, the observed evolution of the "Greenium," (the yield differential between Green Bonds and conventional bonds) has diminished and is currently approaching parity. As of 29th February 2024, the greenium was, on average, around 2bps in the EUR Green Bond Market.

Myth 2: Green Bonds are for niche investors

While this may have been more accurate during the nascent stages of the market a decade ago, it is now an outdated assumption. The green bond market has experienced exceptional growth in recent years, characterised by an expanding issuer base and enhanced liquidity which has resulted in greater sector and regional diversification. The green bond universe has also seen increasing diversification in the credit portion of the market, as well as the growing share of sovereigns.

This evolution, coupled with growing awareness of the necessity to transition to a low-carbon economy, presents attractive investment opportunities, and helps position green bonds as a credible component of the global allocation for the majority of investors.

Myth 3: Green Bond market is relatively small

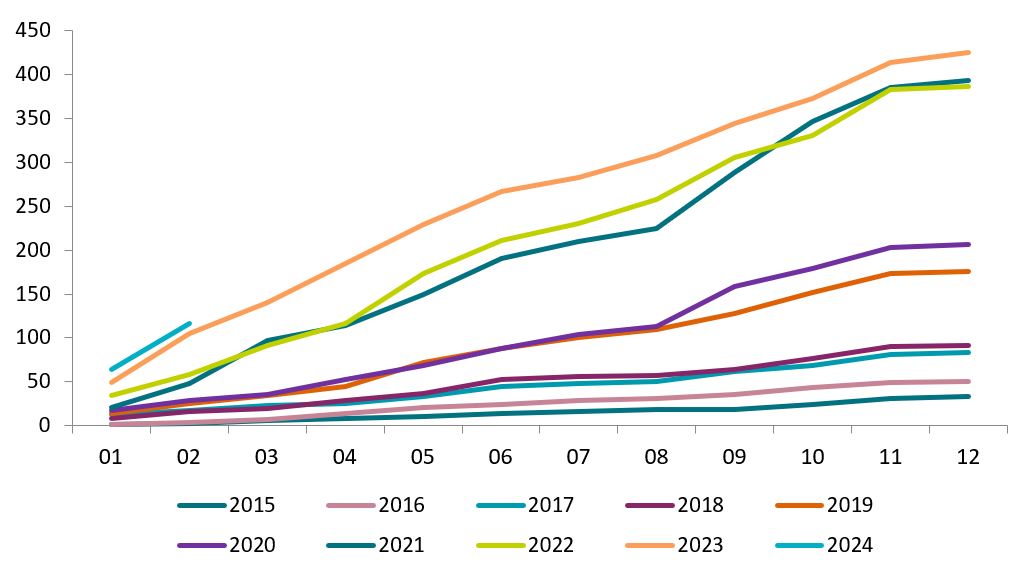

The green bond market has undergone extraordinary expansion in the last decade with a growing number of issuers from the corporate, governmental, and institutional sectors. As the chart shows, even in the challenging market conditions of 2023, issuances of green bonds hit record highs at $422bn of issuances

Volume of green bond issuances per year (in USD bn)

Source: AXA IM, Bloomberg as of 29th February 2024

We have seen a clear shift in interest from more “conventional” investors during the past few years. We expect this interest to continue as investors look to increase their contribution to positive environmental impacts while aiming to have exposure to a rapidly growing market, with high diversification and increasing liquidity.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.