How to effectively use inflation-linked bonds in a portfolio

KEY POINTS

For the past year, fears over rapidly rising inflation have somewhat receeded and the market’s focus has been elsewhere.

However today it is once again becoming a significant worry. Geopolitics has played a significant role - even before Trump’s tariffs started to create inflationary concerns, inflation was proving stickier and more entrenched than many had expected.

With interest rates falling but inflation still above central banks’ targets, for many investors, particularly those with large cash portfolios, managing inflation is an important consideration.

Inflation in a nutshell

Inflation denotes an ongoing fall in money’s overall purchasing power due to a rise in the general level of prices.

Inflation is estimated using price indices, based on subjective baskets of goods and services; these baskets evolve over time as products on the market and consumers’ interests change.

Depending on the components, there are two categories for inflation:

- Headline (overall) which is subject to cyclical fluctuations

- Core (underlying), more representative of the structural evolution of prices (excludes more volatile elements such as food and energy)

The important point to note about inflation is it reduces the return that conventional bonds can provide, and at times of high inflation, it can potentially lead to negative bond returns in real terms.

The chart below shows the impact different levels of inflation could have on an investor’s initial investment of £100 over time.

This is why investors should think in real terms - the returns after inflation has been taken into account - rather than nominal i.e. the return amount before inflation is accounted for. It is also why many investors choose to hedge against inflation risks.

A tool to hedge against inflation

For investors looking to hedge inflation risk, one option available are inflation linked bonds (ILBs). ILBs are bonds, usually issued by governments, that are indexed to Headline inflation (total inflation including food and energy).

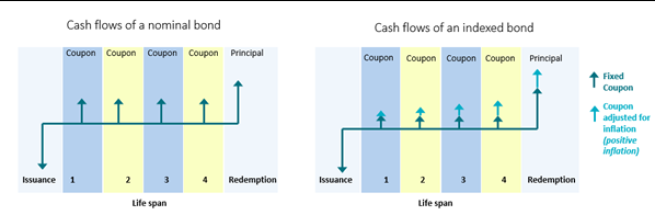

Unlike fixed-rate bonds, the future cash flows of ILBs are not known at the time of purchase as they depend on the future value of the reference inflation index at the fixing date. So rather than a known cashflow, the principal and coupons grow over time thanks to daily indexation process.

As time passes, the value of the principal increases with inflation. Apart from the UK and Canada, the nominal value of an ILBs is also guaranteed at par to protect against deflation.

How does this work for income streams

Coupons, the income paid during the life of a bond, are paid in real terms, providing protection against inflation risk. The amount is computed as a fixed percentage of the inflation-indexed nominal value

This allows the coupon to be constant in real terms. On payment date, the notional is multiplied by the inflation index ratio (index at payment date/index at issue date). So as the reference index rises, the notional of the bond rises proportionally. The investor is therefore paid the fixed real coupon multiplied by the inflation notional..

As inflation indexation is guaranteed by the issuer, the real yield is the annual premium earned on top of realised inflation. However, unlike the principal, there is no protection of the coupon against deflation (except Australia where it is protected).

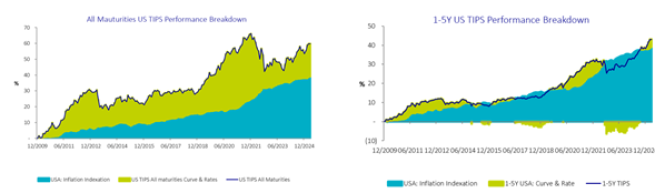

Understanding the performance of all maturities and short duration

Depending on needs and the market environment, investors can choose between all maturities and short duration ILBs.

The chart below highlights the different performance drivers of an all-maturities universe (left-hand chart) versus a short-maturities universe (right-hand chart):

For all maturities, like any other bonds, they are subject to interest rate risks and therefore tend to perform better in stable and low-interest rate environments. Historically, they have performed best in the later stages of an economic cycle.

Short duration ILBs have grown in popularity as all ILBs from a given issuer are indexed to the same inflation rate, irrespective of duration. Therefore, investors looking to hedge inflation without too much exposure to duration, tend to opt for short duration ILBs.

For investors seeking to hedge inflation, ILBs offer an effective solution by locking in positive real yields at the time of purchase while ensuring that future returns are indexed to realised inflation.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.